Financial pressure is becoming a reality for many Canadians. Rising living costs, high interest rates, and unexpected life events can quickly push people into situations where debt begins to feel unmanageable. Credit card balances grow, loan payments pile up, and collection calls may start appearing more frequently than anyone would like. For individuals facing these challenges, understanding available debt relief options becomes essential. One option that many Canadians explore is a consumer proposal, a legal debt solution that allows individuals to negotiate repayment of a portion of their debt while avoiding bankruptcy.

What makes this option particularly important is its potential impact on long-term financial stability. A consumer proposal can help stop collection pressure, reduce the total amount owed, and create a structured path toward rebuilding credit. However, like any financial decision, it requires a clear understanding of how it works, when it makes sense, and how it affects your credit profile. This guide explains the fundamentals of consumer proposals in Canada, how they work, and what individuals should know before considering this type of debt solution.

What is a Consumer Proposal in Canada

A consumer proposal is a formal agreement between a debtor and their creditors to repay a portion of outstanding unsecured debts over time. This process is regulated under the Bankruptcy and Insolvency Act of Canada, ensuring that it follows strict legal guidelines designed to protect both creditors and individuals seeking relief.

Unlike informal debt settlements, a consumer proposal must be filed through a Licensed Insolvency Trustee, who oversees the negotiation and repayment arrangement.

Definition of a Consumer Proposal

A consumer proposal allows individuals to negotiate a reduced repayment amount for unsecured debts while maintaining a structured payment plan.

Key characteristics include:

- The agreement is legally binding once accepted by creditors

- Payments are typically spread over a period of up to five years

- Interest on included debts stops immediately after filing

- Collection actions and legal proceedings must cease once the proposal is filed

For many Canadians, this option provides a middle ground between attempting to manage overwhelming debt alone and declaring bankruptcy.

Types of Debt That Can Be Included

A consumer proposal generally applies to unsecured debts, which are debts not tied to specific collateral.

Common debts included in a proposal may involve:

- Credit card balances

- Personal loans

- Lines of credit

- Payday loans

- Tax debt owed to the Canada Revenue Agency

- Certain unsecured business debts

However, secured debts typically remain separate. For example:

- Mortgages

- Car loans tied to financed vehicles

Student loans may also qualify under specific circumstances if the borrower has been out of school for several years.

Understanding which debts can be included helps determine whether a consumer proposal will effectively address an individual’s financial situation.

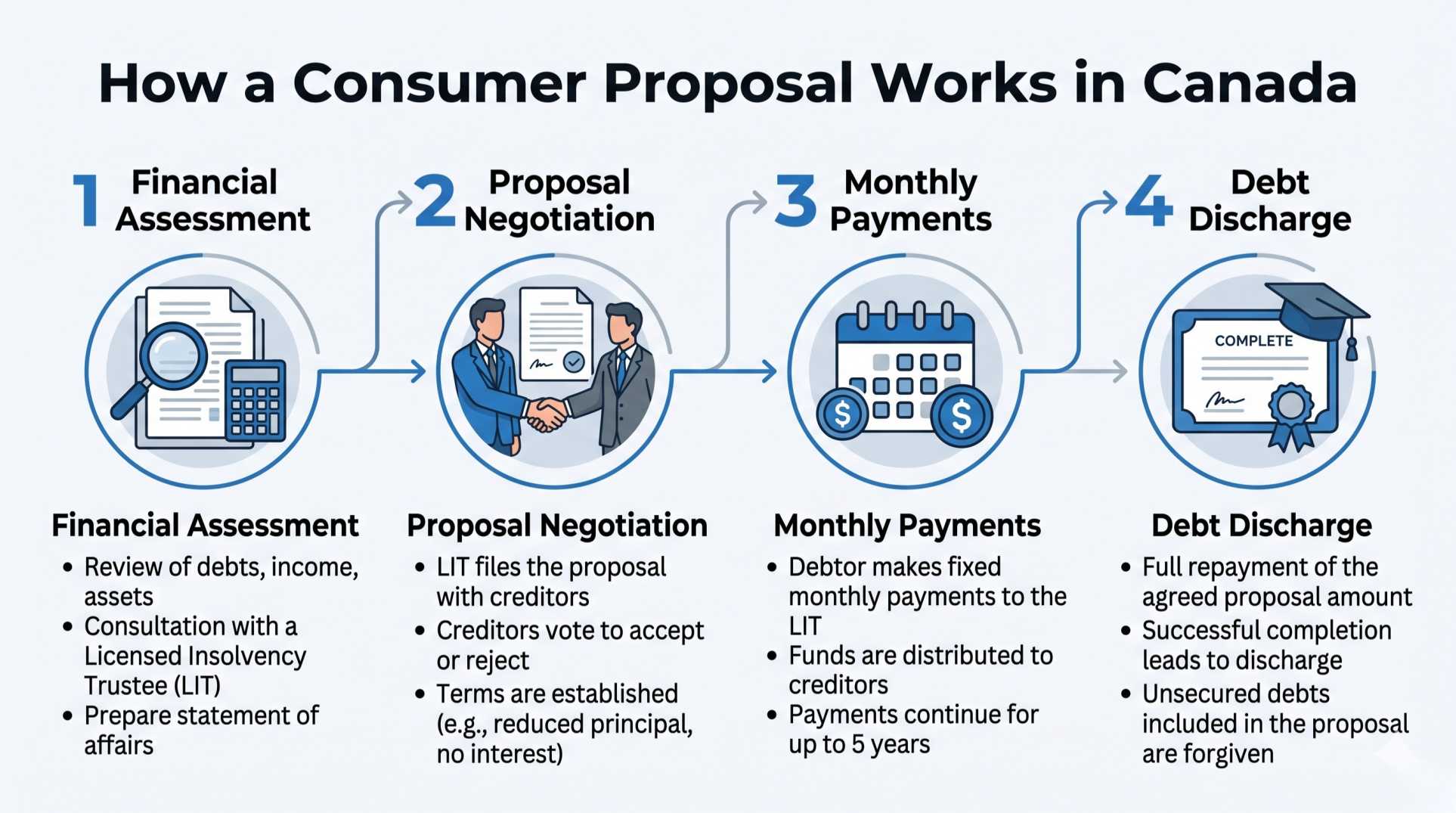

How a Consumer Proposal Works Step by Step

The consumer proposal process follows a structured series of steps designed to evaluate financial circumstances and negotiate repayment terms with creditors.

Step 1: Financial Assessment

The process begins with a thorough financial review.

This assessment examines:

- Total outstanding debt

- Income sources and monthly expenses

- Current financial obligations

- Long-term repayment ability

A Licensed Insolvency Trustee evaluates whether a consumer proposal is the most appropriate option or whether alternative solutions may be more suitable.

Step 2: Proposal Creation and Negotiation

Once the financial review is complete, the trustee prepares a formal proposal for creditors.

The proposal typically offers creditors a repayment amount that is lower than the total debt but higher than what they might recover through bankruptcy.

Key elements include:

- A reduced total repayment amount

- A structured monthly payment schedule

- A maximum repayment period of five years

Creditors then review the proposal and vote on whether to accept it.

If creditors representing more than half of the total debt value approve, the proposal becomes legally binding for all included creditors.

Step 3: Monthly Repayment Period

After approval, the individual begins making fixed monthly payments according to the agreed plan.

Important features during this stage include:

- No additional interest is added to the included debts

- Payment amounts remain consistent throughout the term

- Creditors cannot pursue further collection activity

This predictable repayment structure allows individuals to regain control over their finances.

Step 4: Completion and Debt Discharge

Once all payments are completed, the remaining debt included in the proposal is legally forgiven.

At this stage, the individual receives a Certificate of Full Performance, confirming successful completion of the agreement.

For many Canadians, this marks the beginning of a new financial chapter with significantly reduced debt obligations.

How a Consumer Proposal Affects Your Credit Score

A common concern for individuals considering a consumer proposal is how it will affect their credit profile.

While there is an impact, understanding the details can help people plan their credit recovery effectively.

Credit Rating Assigned to a Consumer Proposal

When a consumer proposal is filed, it is recorded on credit reports with an R7 rating.

This rating indicates that debts are being repaid through a formal settlement agreement.

The record typically remains on credit reports for:

- Three years after the proposal is completed

- Or six years from the filing date, whichever occurs first

Although this may temporarily lower a credit score, it often stabilizes financial conditions by eliminating growing interest charges and collection pressure.

Rebuilding Credit During the Proposal

Credit rebuilding can begin even before the proposal is completed.

Steps that support credit recovery include:

- Making all proposal payments on time

- Paying remaining financial obligations consistently

- Using secured credit products responsibly

These actions help demonstrate financial responsibility to future lenders.

Long Term Credit Recovery

Many Canadians gradually rebuild their credit within a few years after completing a consumer proposal.

With responsible financial habits, individuals may regain eligibility for:

- Personal loans

- Credit cards

- Mortgage financing

The key factor is consistent financial discipline following debt resolution.

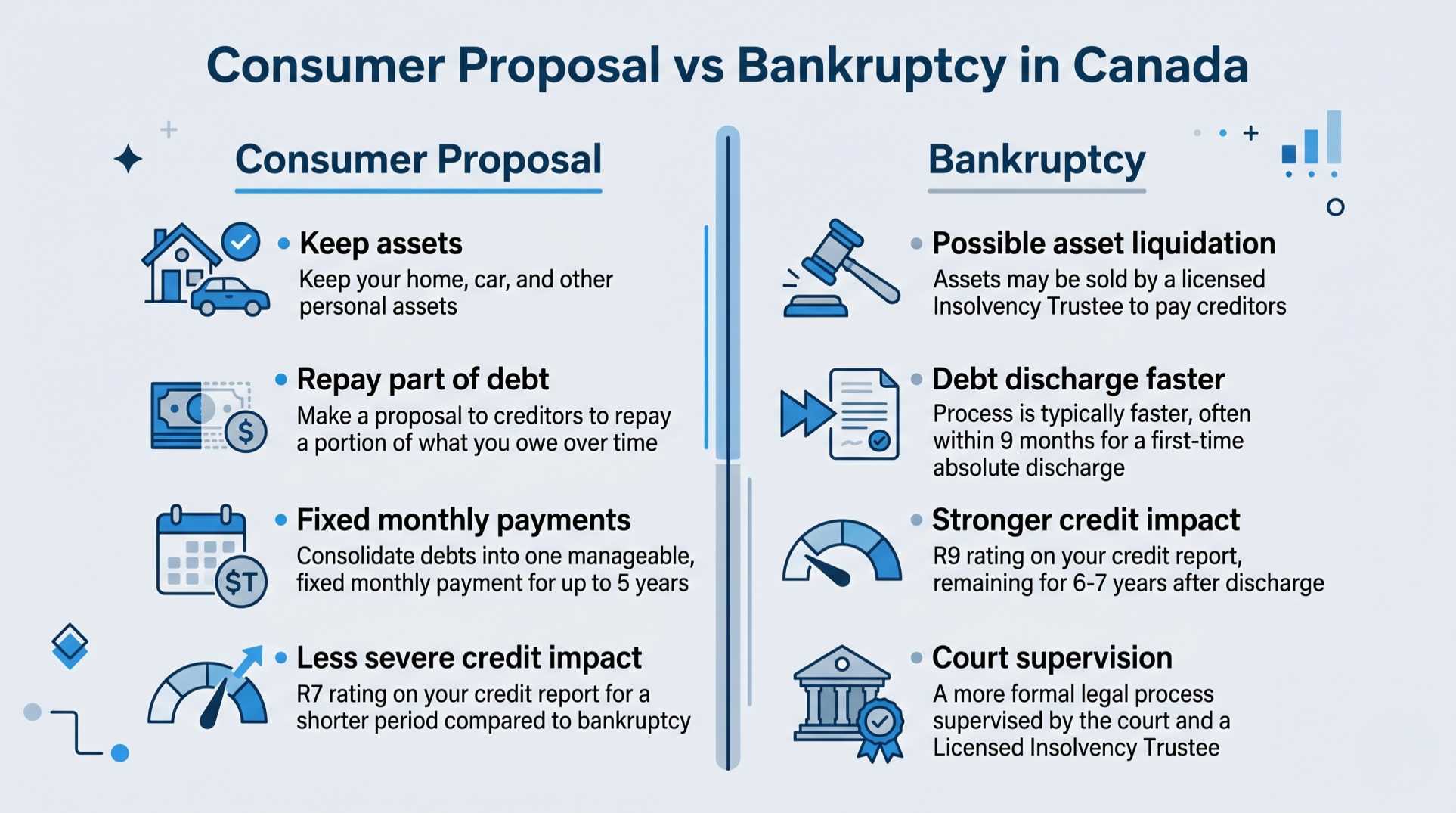

Consumer Proposal vs Bankruptcy

Understanding the difference between a consumer proposal and bankruptcy helps individuals choose the option that best fits their financial circumstances.

Key Differences Between the Two Options

Bankruptcy and consumer proposals both provide legal debt relief, but they operate differently.

Bankruptcy may involve:

- Potential liquidation of certain assets

- A shorter but more severe impact on credit

- Court-supervised debt discharge

Consumer proposals typically allow individuals to:

- Keep their assets

- Repay a portion of their debt over time

- Avoid many of the long-term consequences associated with bankruptcy

Situations Where a Consumer Proposal May Be Better

A consumer proposal may be more appropriate when:

- The individual has a stable income

- Total unsecured debt has become difficult to manage

- The person wants to avoid asset liquidation

- Monthly payments can still be maintained at a reduced level

In these cases, a proposal offers a structured compromise between full repayment and bankruptcy.

Benefits of a Consumer Proposal

Consumer proposals offer several advantages that make them an attractive option for many individuals dealing with high debt levels.

Financial Advantages

Some of the most significant financial benefits include:

- Reduction in total debt owed

- Elimination of ongoing interest charges

- Legal protection from wage garnishment

- Immediate stop to collection calls

These benefits can significantly ease financial pressure.

Psychological and Lifestyle Benefits

Financial stress often affects mental well-being and personal relationships.

A structured debt solution can provide:

- Clear repayment expectations

- Reduced anxiety related to debt collectors

- Greater financial predictability

- Renewed focus on long-term financial planning

Many individuals find that this clarity helps restore confidence in managing their finances.

Common Myths About Consumer Proposals

Despite their benefits, consumer proposals are often misunderstood.

Myth: Consumers Lose All Their Assets

In reality, most people keep their major assets, such as homes and vehicles, as long as payments remain current.

Myth: It Permanently Ruins Credit

While a consumer proposal does affect credit temporarily, many individuals rebuild strong credit profiles after completing the agreement.

Myth: Only People in Severe Debt Qualify

Consumer proposals are not limited to extreme financial situations. They are often used by individuals with stable income who simply need a manageable repayment structure.

Common Mistakes People Make When Considering a Consumer Proposal

Understanding potential pitfalls helps individuals make more informed financial decisions.

Waiting Too Long to Seek Help

Many people delay addressing debt issues until financial pressure becomes overwhelming.

Seeking advice early can prevent:

- Escalating interest charges

- Collection activity

- Legal enforcement actions

Not Reviewing All Debt Relief Options

Consumer proposals are just one option within the broader landscape of debt solutions.

Other possibilities may include:

- Debt consolidation loans

- Credit counselling programs

- Informal repayment negotiations

Professional guidance can help determine which option best fits individual circumstances.

Ignoring Long-Term Financial Habits

Debt solutions resolve immediate financial pressure, but long-term financial stability depends on improved money management.

Key habits include:

- Budgeting consistently

- Limiting unnecessary credit use

- Maintaining emergency savings

Expert Tips for Improving Your Credit After a Consumer Proposal

Once debt has been reduced or eliminated, rebuilding credit becomes a priority.

Build a Strong Payment History

Credit scores rely heavily on payment consistency.

Important habits include:

- Paying all bills on time

- Avoiding missed payments

- Maintaining low credit utilization levels

Start With Secured Credit Products

Secured credit cards often provide a safe starting point for rebuilding credit.

Responsible use demonstrates improved financial behavior to lenders.

Monitor Credit Reports Regularly

Reviewing credit reports helps identify errors and track progress.

Canadians can monitor reports through major credit bureaus such as:

- Equifax

- TransUnion

Correcting inaccuracies ensures that credit history reflects true financial performance.

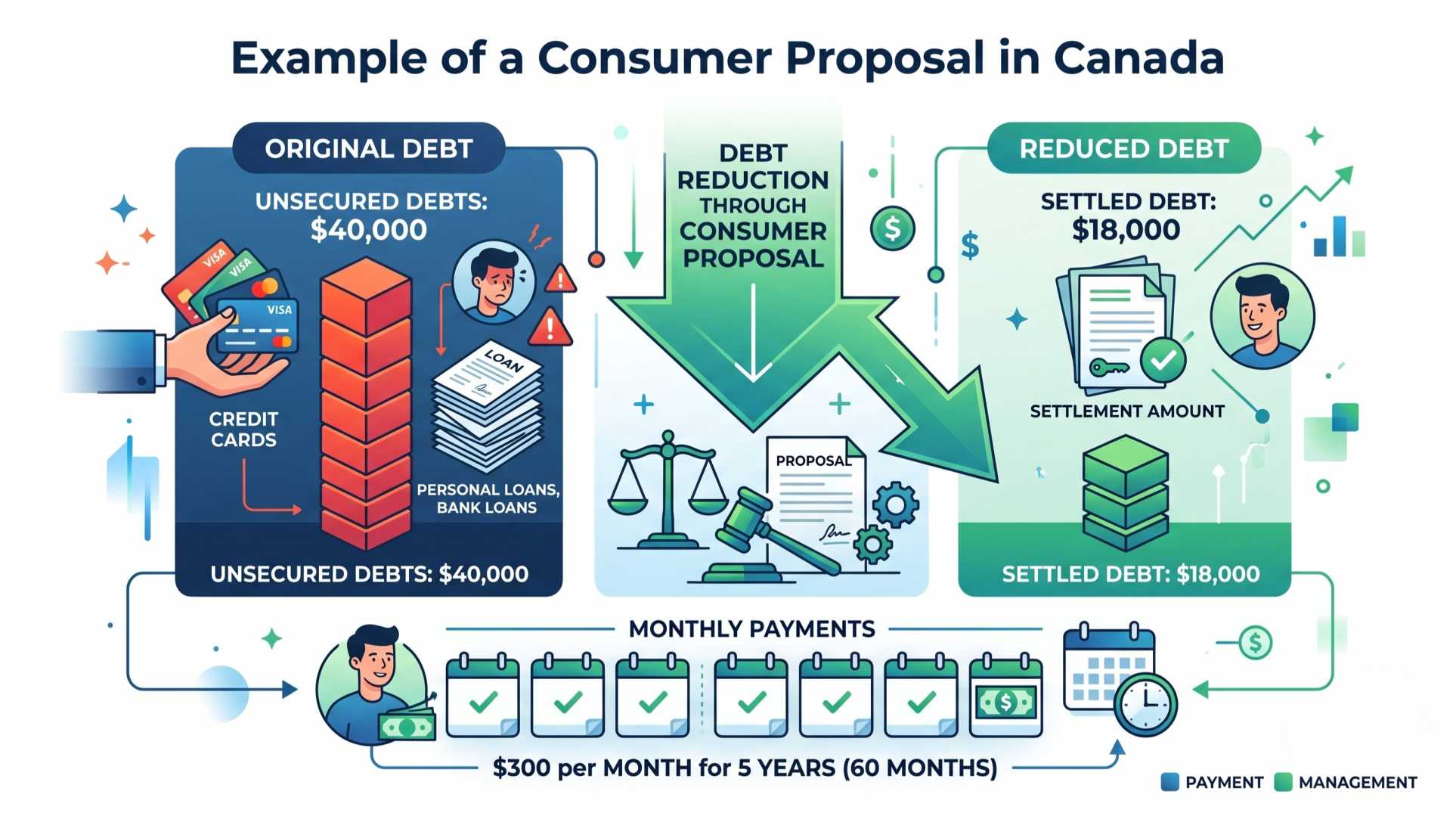

Real Life Example of a Consumer Proposal

Consider a typical scenario faced by many Canadians.

An individual accumulates several debts over time:

- Credit card balances

- Personal loans

- Line of credit payments

The total unsecured debt reaches 40,000 dollars, making monthly payments increasingly difficult.

After reviewing their financial situation, a consumer proposal is negotiated.

The agreement reduces the total repayment amount to 18,000 dollars, payable at 300 dollars per month over five years.

Through this structured arrangement:

- Interest stops accumulating

- Creditors stop collection activity

- The individual saves more than half the original debt amount

This example illustrates how a consumer proposal can create a manageable pathway toward financial recovery.

FAQs

What is the minimum debt required for a consumer proposal in Canada?

There is no fixed minimum debt requirement. However, proposals are typically considered when unsecured debts become difficult to manage.

Can I keep my home if I file a consumer proposal?

In most cases, yes, provided mortgage payments remain current and the property remains affordable.

Does a consumer proposal stop collection calls?

Yes. Once filed, creditors must stop collection actions and legal proceedings related to the included debts.

Can I pay off a consumer proposal early?

Yes. Many individuals choose to complete their repayment earlier if their financial situation improves.

What is the difference between a consumer proposal and debt settlement in Canada?

A consumer proposal is a legal debt agreement filed through a Licensed Insolvency Trustee, while debt settlement is an informal negotiation with creditors. A consumer proposal also provides legal protection from collections.

Does a consumer proposal stop collection calls?

Yes. Once a consumer proposal is officially filed, creditors must stop collection calls, wage garnishments, and legal actions related to the debts included in the proposal. This protection is provided under Canadian insolvency law.

How long does a consumer proposal stay on a credit report?

A consumer proposal typically remains on your credit report for three years after it is completed or six years from the date it was filed, whichever happens first.

Can I get a mortgage after a consumer proposal?

Yes, it is possible to get a mortgage after completing a consumer proposal. Many lenders require borrowers to rebuild their credit, maintain a stable income, and show a history of responsible financial behavior before approving a mortgage application.

What happens if creditors reject a consumer proposal?

If creditors reject the proposal, the Licensed Insolvency Trustee may revise the terms and negotiate a new agreement that creditors are more likely to accept. If an agreement cannot be reached, other debt relief options may need to be considered.

Does a consumer proposal affect employment in Canada?

In most cases, a consumer proposal does not affect employment. Employers are generally not notified unless wage garnishment was previously involved or the job requires specific financial background checks.

Conclusion

Managing overwhelming debt can feel stressful and uncertain, but Canadians have several structured options available to regain financial control. A consumer proposal offers a legally recognized way to reduce unsecured debt while avoiding bankruptcy and protecting important assets.

By understanding how the process works, individuals can make informed decisions about their financial future. Structured repayment plans, responsible financial habits, and consistent credit rebuilding can gradually restore stability and confidence.

For those unsure about the best path forward, seeking guidance from experienced credit professionals can provide clarity. Organizations such as Credit 720 help Canadians explore practical debt solutions, improve credit profiles, and work toward long-term financial health.