Debt problems rarely happen overnight. For many Canadians, financial stress begins with small issues like missed payments, rising credit card balances, or unexpected expenses. Over time, these problems can grow into a situation where managing monthly payments becomes extremely difficult. If you’re dealing with mounting debt, collection calls, or declining credit scores, you’re not alone. Many Canadians face similar financial challenges every year. The key is recognizing the warning signs early and understanding the solutions available.

One option that can help individuals regain control of their finances is a consumer proposal. It allows people struggling with unsecured debt to negotiate a manageable repayment plan while protecting themselves from creditor actions. Organizations like Credit 720 help Canadians better understand their financial options, including whether a Canadian consumer proposal could be a suitable step toward financial recovery.

What Is a Consumer Proposal?

A consumer proposal is a legally binding agreement between you and your creditors that allows you to repay a portion of your debt over time.

It is regulated under Canadian insolvency laws and must be filed through a Licensed Insolvency Trustee.

Instead of paying the full amount you owe, creditors may agree to accept reduced payments based on your financial situation.

Key benefits include:

- Lower total debt repayment

- One manageable monthly payment

- Interest on eligible debts stops accumulating

- Protection from collection calls and legal action

- A structured path toward rebuilding credit

Many Canadians consult financial guidance providers like Credit 720 to better understand consumer proposal requirements and determine whether this solution fits their financial situation.

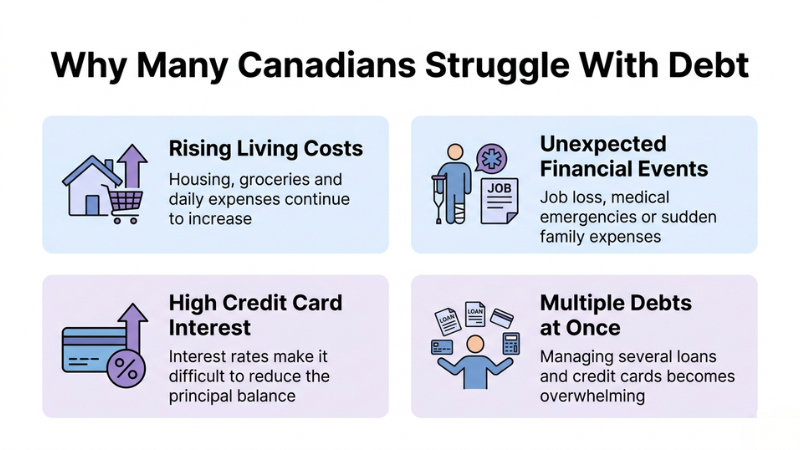

Why Many Canadians Struggle With Debt

Debt challenges can arise for several reasons, and they often develop gradually.

Rising Living Costs

Housing, groceries, transportation, and other daily expenses continue to increase across Canada. As living costs rise, many households rely more heavily on credit to maintain their financial stability.

Unexpected Financial Events

Job loss, medical issues, or family emergencies can disrupt even well-planned finances. When savings are limited, people may turn to credit cards or personal loans to manage these expenses.

High Credit Card Interest

Credit cards often carry high interest rates. When balances grow large, it becomes difficult to pay off the principal, causing debt to increase over time.

Multiple Debts at Once

Managing several credit cards, loans, and lines of credit can quickly become overwhelming. Missing even one payment can negatively affect credit scores and lead to collection activity.

Financial educators at Credit 720 frequently see individuals facing these situations before exploring formal debt solutions.

Signs You May Need a Consumer Proposal

Recognizing the warning signs early can help prevent deeper financial problems. Here are several indicators that a Canadian consumer proposal may be worth considering.

1. You Are Only Making Minimum Payments

If you are consistently paying only the minimum balance on your credit cards and your total debt is not decreasing, it may be a sign that your debt is becoming difficult to manage.

2. Collection Calls Are Increasing

Frequent calls or letters from creditors or collection agencies indicate overdue accounts. A consumer proposal can legally stop most collection activities once it is filed.

3. Your Debt Is Too Large for Your Income

When your monthly debt payments take up a significant portion of your income, it becomes difficult to maintain financial stability.

4. You Are Using Credit to Pay Other Debts

Using one credit card to pay another or taking new loans to cover existing debts can lead to a cycle that becomes increasingly difficult to escape.

5. Your Credit Score Is Declining

Missed payments, high credit utilization, and accounts in collections can significantly reduce your credit score.

Financial advisors often recommend reviewing options like a consumer proposal when these signs appear. Many individuals explore guidance from services such as Credit 720 to better understand their next steps.

Practical Steps to Improve Financial Stability

Before deciding on any debt solution, it’s important to understand your financial position and take steps to regain control.

Review Your Credit Report

Checking your credit report helps you identify outstanding debts, missed payments, and any errors that may affect your credit score.

Create a Realistic Budget

A well-structured budget can help prioritize essential expenses and debt payments.

Your budget should include:

- Fixed monthly expenses

- Variable spending

- Debt obligations

- Savings contributions

Financial guidance resources such as Credit 720 often emphasize budgeting as a critical step toward improving financial health.

Reduce High-Interest Debt

If possible, prioritize paying down high-interest debt first. This can reduce the amount of interest you pay over time and help accelerate debt repayment.

Avoid New Credit Applications

Opening new credit accounts while managing existing debt can worsen your financial situation. Focus on stabilizing current obligations first.

Common Credit Mistakes to Avoid

When trying to improve financial health, certain mistakes can unintentionally damage your credit profile.

Closing Old Credit Accounts

Older accounts contribute to your credit history length. Closing them may reduce your credit score.

Ignoring Credit Reports

Regularly reviewing your credit report helps detect inaccuracies or fraudulent activity.

Applying for Multiple Loans

Submitting several credit applications within a short period can negatively affect your credit score.

Missing Payments

Payment history is one of the most important factors influencing credit scores. Even one missed payment can have a lasting impact.

Financial education programs, including those supported by Credit 720, often focus on helping individuals avoid these common credit mistakes.

How Credit 720 Supports Canadians Managing Debt

Recovering from debt requires both financial planning and reliable guidance.

Organizations like Credit 720 help Canadians better understand their financial options and make informed decisions about improving their credit and managing debt.

Support typically includes:

- Credit education and financial guidance

- Debt management insights

- Information about consumer proposal requirements

- Strategies for rebuilding credit

- Long-term financial planning resources

By focusing on education and responsible financial strategies, Credit 720 helps individuals move toward long-term financial stability.

FAQs

What is a Canadian consumer proposal?

A Canadian consumer proposal is a legal agreement that allows individuals to repay a portion of their unsecured debt through manageable monthly payments.

What are consumer proposal requirements in Canada?

To qualify, individuals must have unsecured debts under $250,000 and work with a Licensed Insolvency Trustee to file the proposal.

Does a consumer proposal stop collection calls?

Yes. Once a consumer proposal is filed, creditors must stop most collection actions and communication.

Can I rebuild my credit after a consumer proposal?

Yes. Many Canadians rebuild credit by making payments on time and using credit responsibly after completing the proposal.

Conclusion

Debt challenges can feel overwhelming, but recognizing the warning signs early can help you take meaningful action. If you are struggling with rising balances, frequent collection calls, or declining credit scores, it may be time to explore options like a consumer proposal.

Understanding consumer proposal requirements and reviewing your financial situation can help you choose the best path forward.

With proper guidance and financial education, many Canadians successfully recover from debt and rebuild their credit. Resources like Credit 720 can provide valuable insights and support for individuals looking to improve their financial future.