Many Canadians do not realize how quickly debt can move from manageable to stressful. One month, it may be a credit card balance that is a little higher than usual. A few months later, it may become missed payments, payday loans, overdraft use, collection calls, and loan rejection.

This is where credit counselling can help. It gives people a clearer look at what they owe, what they can afford, and which repayment path makes sense before the situation becomes harder to control.

For someone with poor credit, maxed-out cards, high-interest debt, or difficulty getting approved for loans, the first step is not always taking another loan. Sometimes the smarter move is understanding the full financial picture first.

Credit counselling connects budgeting, credit reports, debt repayment, lending approval, and long-term credit recovery. With the right guidance, Canadians can make better decisions about debt consolidation, consumer proposals, repayment planning, and future financial stability.

What Is Credit Counselling

Simple Definition

Credit counselling is a financial guidance service that helps people review their income, expenses, debts, credit accounts, and repayment options.

A credit counsellor may help you understand where your money is going, which debts are creating the most pressure, and what type of plan may fit your current income.

It can include support with budgeting, debt repayment planning, creditor communication, and education about credit reports. The goal is not only to deal with debt today, but also to help prevent the same problems from returning later.

For many Canadians, this process is the first serious step toward financial clarity. It turns a confusing debt situation into a structured plan.

What Credit Counselling Is Not

Credit counselling is not a quick credit score fix.

It is not the same as taking a new loan. It also does not automatically mean you are filing a consumer proposal or bankruptcy.

A trustworthy counselling process should never promise instant debt removal, guaranteed credit approval, or overnight score improvement. Credit recovery takes time, consistency, and the right repayment strategy.

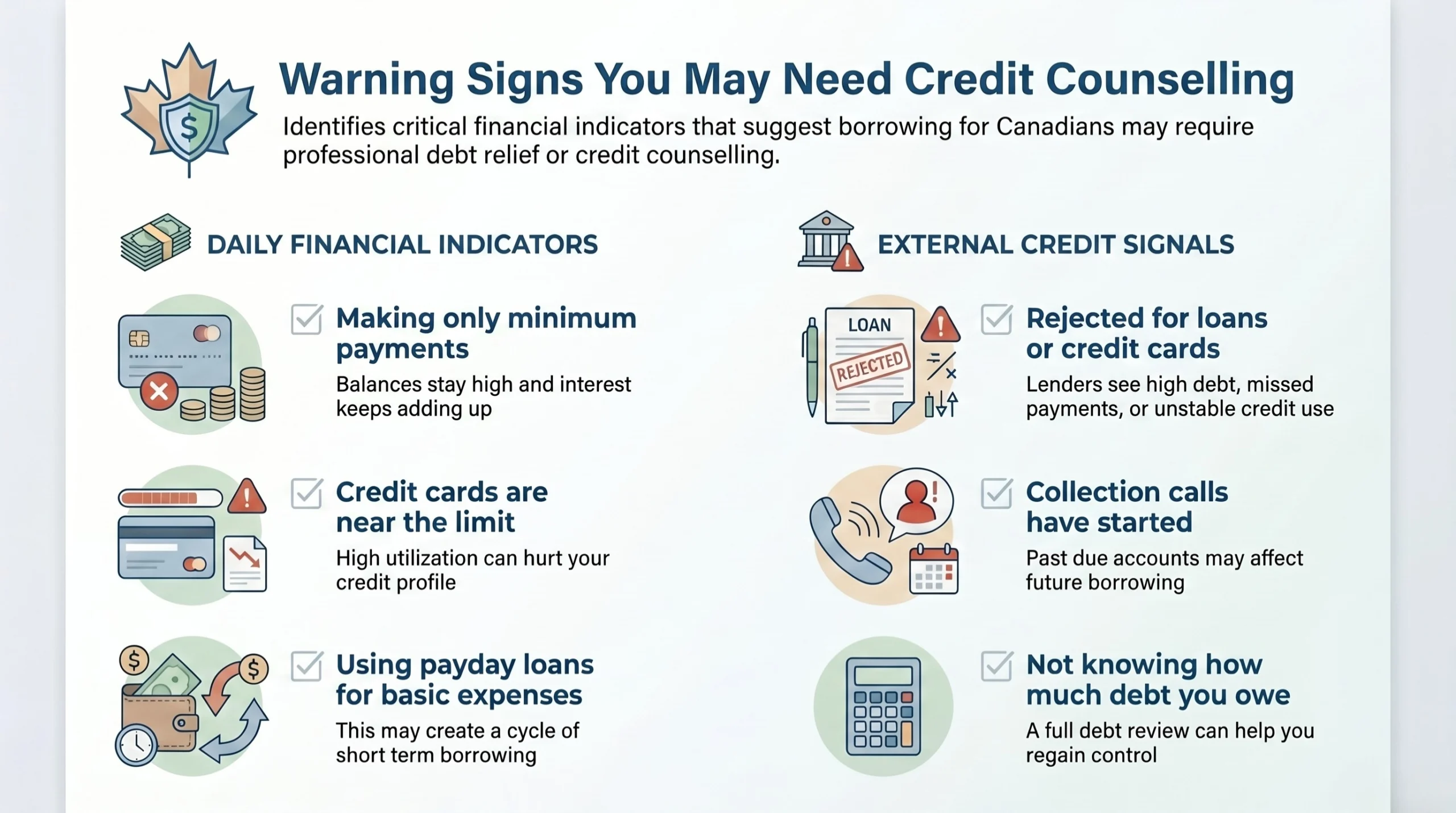

Who Usually Needs Credit Counselling

Credit counselling may be useful if you are dealing with any of these situations.

- Credit card balances that are not going down

- Minimum payments that barely cover interest

- Loan, mortgage, or credit card rejection

- Payday loans are used to cover basic expenses

- Overdraft or line of credit use every month

- Collection calls or past due accounts

- Confusion about debt consolidation, consumer proposal, or bankruptcy

If debt is affecting your sleep, relationships, or confidence, it may be time to get help before the options become more limited.

Why Credit Counselling Matters for Canadians With Poor Credit

It Helps Identify the Real Cause of Credit Problems

A low credit score is usually a symptom. The real cause may be high-interest debt, missed payments, lack of budgeting, unstable income, or overuse of revolving credit.

For example, someone may think missed payments are the main problem. After reviewing the full situation, they may discover that their credit card utilization is too high and their monthly cash flow leaves no room for emergency expenses.

Credit counselling helps separate short-term cash flow pressure from long-term debt overload. This matters because each situation needs a different solution.

Someone with a temporary budget issue may need expense control and payment planning. Someone with unmanageable unsecured debt may need a more formal debt solution.

It Can Improve Loan Readiness Over Time

Lenders do not only look at your credit score. They also review payment history, debt load, credit utilization, income stability, and recent credit activity.

Credit counselling can help reduce risky financial habits before you apply for a loan, mortgage, or new credit card.

This may include paying bills on time, lowering credit card balances, avoiding repeated applications, and building a more stable payment record.

Better loan readiness does not happen overnight. But a clear plan can help you move from rejection risk toward stronger financial credibility.

It Reduces Financial Confusion

Many Canadians are unsure about the difference between credit counselling, debt consolidation, consumer proposal, and bankruptcy.

That confusion can lead to rushed decisions. Some people take a high-interest consolidation loan when they cannot afford the payment. Others delay getting help until collections or legal pressure begin.

Credit counselling helps you compare options in plain language. It is useful for people who are just becoming aware of the problem and for those already deciding between debt relief paths.

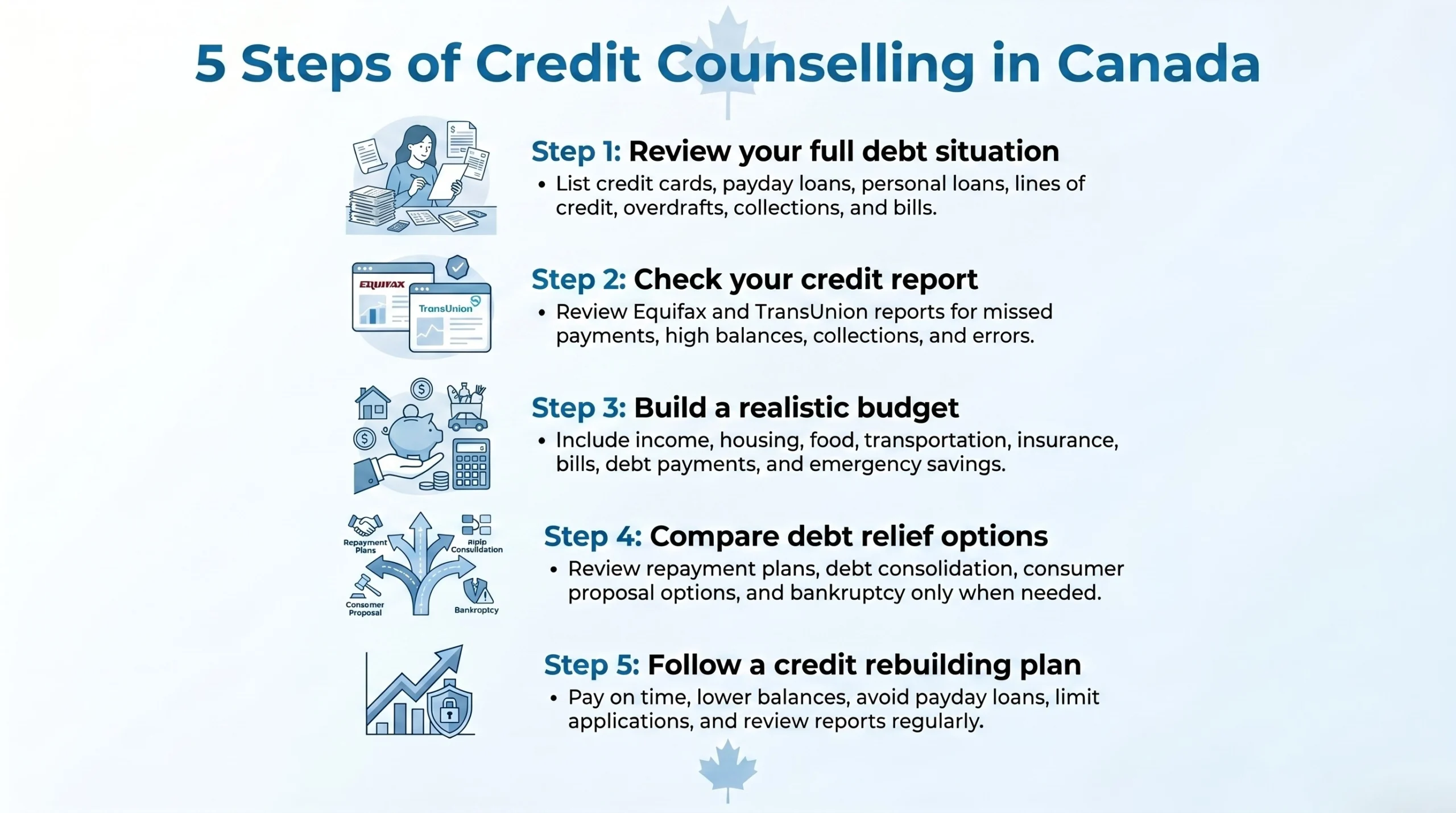

How Credit Counselling Works Step by Step

Step 1: Review Your Full Financial Situation

The first step is to list every unsecured debt. This may include credit cards, payday loans, personal loans, lines of credit, overdrafts, collection accounts, and unpaid bills.

You also need to review monthly income, fixed expenses, variable spending, and missed payment history.

This gives you a realistic view of your financial position. Many people feel anxious before doing this, but the numbers often bring relief because they finally know what they are dealing with.

Step 2: Understand Your Credit Report

Your credit report shows how you have managed credit accounts over time.

Missed payments, high balances, collection accounts, and hard inquiries can affect your credit profile. That is why it is important to review both Equifax and TransUnion reports in Canada.

A credit report review can help identify errors, outdated information, duplicate accounts, or collections that need attention.

This step is important because rebuilding credit starts with knowing what lenders can see.

Step 3: Build a Realistic Budget

A budget should show what you can actually afford to pay each month.

It should include housing, food, transportation, insurance, childcare, loan payments, utilities, and emergency savings.

The goal is not only to reduce existing debt. The goal is to stop new debt from forming.

A good budget should feel practical, not punishing. If the plan is too strict, most people cannot follow it for long.

Step 4: Compare Debt Relief Options

After reviewing the numbers, the next step is comparing possible solutions.

Credit counselling may lead to a structured repayment plan. Debt consolidation may help if the borrower qualifies for better terms and can afford the new payment.

A consumer proposal may be considered when unsecured debt is no longer manageable. It can reduce what a person pays back and extend repayment through a formal legal process.

Bankruptcy may be a last resort when other solutions are not realistic.

Credit 720 supports Canadians by helping them understand debt consolidation, credit counselling, consumer proposal-related guidance, budgeting, and debt management options practically.

Step 5: Follow a Credit Rebuilding Plan

Once the repayment path is clear, the next step is credit rebuilding.

Focus on these habits.

- Make payments on time

- Keep credit card balances low

- Avoid payday loans

- Avoid repeated credit applications

- Review credit reports regularly

- Build emergency savings

- Keep older positive accounts in good standing where possible

Credit rebuilding is not about one big move. It is about repeated small actions that show lenders you can manage credit responsibly.

Credit Counselling and Your Credit Score

Does Credit Counselling Hurt Your Credit Score

Speaking with a counsellor does not directly damage your credit score.

The impact depends on what solution you choose after counselling. A debt management plan, consumer proposal, missed payments, or settled accounts may appear differently on a credit report.

This is why it is important to ask how each option may affect your credit file before making a decision.

What Actually Affects Your Score

Several factors can influence your credit score.

- Payment history

- Credit utilization

- Length of credit history

- Credit mix

- New credit applications

- Collections or insolvency-related information, where applicable

Payment history and credit utilization are especially important. Paying late and keeping cards near the limit can make it harder to qualify for affordable credit.

How Counselling Can Support Credit Repair

Credit counselling can support credit repair by creating a payment strategy and reducing reliance on high-interest borrowing.

It can also help organize past due accounts, explain better credit use, and prepare borrowers before applying for new credit.

The counselling process does not erase accurate negative information. Instead, it helps you build a cleaner path forward.

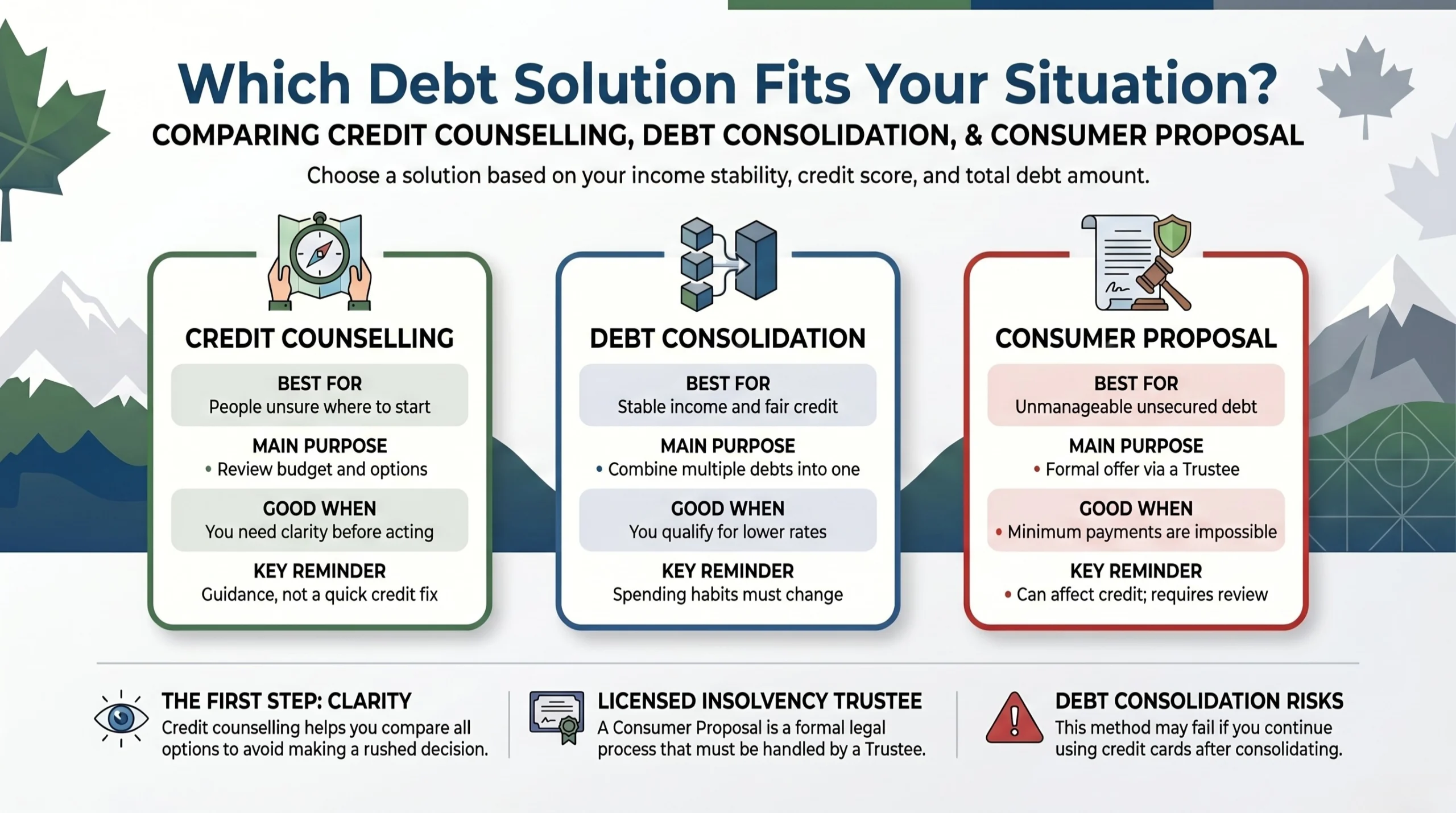

Credit Counselling vs Debt Consolidation

What Debt Consolidation Means

Debt consolidation means combining multiple debts into one payment.

For example, someone with three credit cards, one personal loan, and one payday loan may try to combine them into a single monthly payment.

This can simplify finances if the interest rate is lower and the new payment is affordable.

When Debt Consolidation May Help

Debt consolidation may work well when the borrower has a stable income and can qualify for a reasonable interest rate.

It may also help if the person has not already missed too many payments and the monthly payment fits comfortably within the budget.

The keyword is affordable. A consolidation loan that creates another stressful payment may only delay the problem.

When Credit Counselling May Be Better First

Credit counselling may be better before consolidation if you are unsure what you can afford.

It may also help if your credit score is poor, your debt includes payday loans or collections, or your spending habits need to be fixed before taking a new loan.

Without a budget review, consolidation can become a cycle. The person pays off credit cards with a loan, then uses the cards again because the root issue was never solved.

Credit Counselling vs Consumer Proposal

What a Consumer Proposal Is

A consumer proposal is a formal legal debt solution in Canada.

It allows an eligible person to make an offer to repay part of their unsecured debt through a Licensed Insolvency Trustee. The repayment is usually structured over time.

It can reduce unsecured debt and create a more predictable repayment path when regular payments are no longer manageable.

When a Consumer Proposal May Be Considered

A consumer proposal may be considered when minimum payments are no longer realistic.

It may also be suitable when creditors are calling, legal action is starting, debt consolidation is unavailable, or the borrower wants to avoid bankruptcy, where possible.

This is not a casual decision. It can affect credit, borrowing options, and financial planning for several years.

Why Counselling Before a Proposal Is Useful

Counselling before a proposal helps compare all options.

It can clarify the credit impact, repayment commitment, and long-term consequences. It also reduces the risk of choosing a solution without understanding what happens next.

For many Canadians, the right answer is not obvious until income, expenses, debts, and credit history are reviewed together.

Common Types of Debt Discussed in Credit Counselling

Credit Card Debt

Credit card debt is one of the most common reasons people seek counselling.

High-interest balances can grow quickly, especially when payments only cover a small portion of the principal. Minimum payments may keep the account active, but they often delay real progress.

Counselling can help prioritize payments and reduce balance pressure.

Payday Loans

Payday loans can create a difficult borrowing cycle.

The repayment period is short, and many borrowers end up taking another loan to cover the next expense. This can quickly affect cash flow and credit recovery.

This is where payday loan consolidation or a broader repayment strategy may need to be discussed.

Personal Loans and Lines of Credit

Personal loans and lines of credit need different repayment strategies.

A fixed personal loan has set payments, while a line of credit can keep revolving if the borrower continues to draw from it.

Credit 720 provides educational content around personal loan debt, overdraft, and lines of credit support, which can help borrowers understand how each debt type affects repayment planning.

Collection Accounts

Collection accounts can affect creditworthiness and future approvals.

Before paying or negotiating, borrowers should understand validation, repayment agreements, and how updates may appear on credit reports.

A planned approach is better than reacting under pressure from calls or letters.

Myth vs Fact About Credit Counselling

Myth 1: Credit Counselling Is Only for People Near Bankruptcy

Fact: Credit counselling can help much earlier. It is useful for people struggling with budgeting, credit card balances, payday loans, or loan approval problems.

Myth 2: Credit Counselling Erases Bad Credit Instantly

Fact: It does not erase accurate negative information. It helps build a realistic recovery plan and better financial habits.

Myth 3: Debt Consolidation Is Always Better Than Counselling

Fact: Debt consolidation may fail if the borrower keeps using credit cards or accepts a high-interest loan. Counselling helps check whether consolidation is realistic.

Myth 4: Credit Counselling Means You Failed Financially

Fact: It is a planning tool. Many responsible people use it to regain control before debt becomes worse.

Common Mistakes Canadians Make Before Getting Credit Help

Waiting Too Long

Many people wait until collections, missed payments, or legal notices begin.

Earlier guidance usually gives more options. Waiting can limit access to lower-cost solutions and increase financial stress.

Taking More Credit to Pay Old Credit

Using new credit to pay off old credit can increase risk if income and spending are not fixed first.

This may worsen credit utilization, increase monthly payment pressure, and make future borrowing harder.

Ignoring Credit Reports

Errors, old accounts, and unpaid collections can hurt future approvals.

Reviewing credit reports should be part of the counselling process because it helps identify what needs to be corrected, paid, disputed, or monitored.

Choosing a Debt Relief Company Without Checking Credibility

People under financial stress can become targets for unrealistic promises.

Be careful with companies that guarantee instant results, pressure you to sign quickly, or ask for fees without clearly explaining what they do.

A credible service should explain your options, risks, fees, and credit impact in clear language.

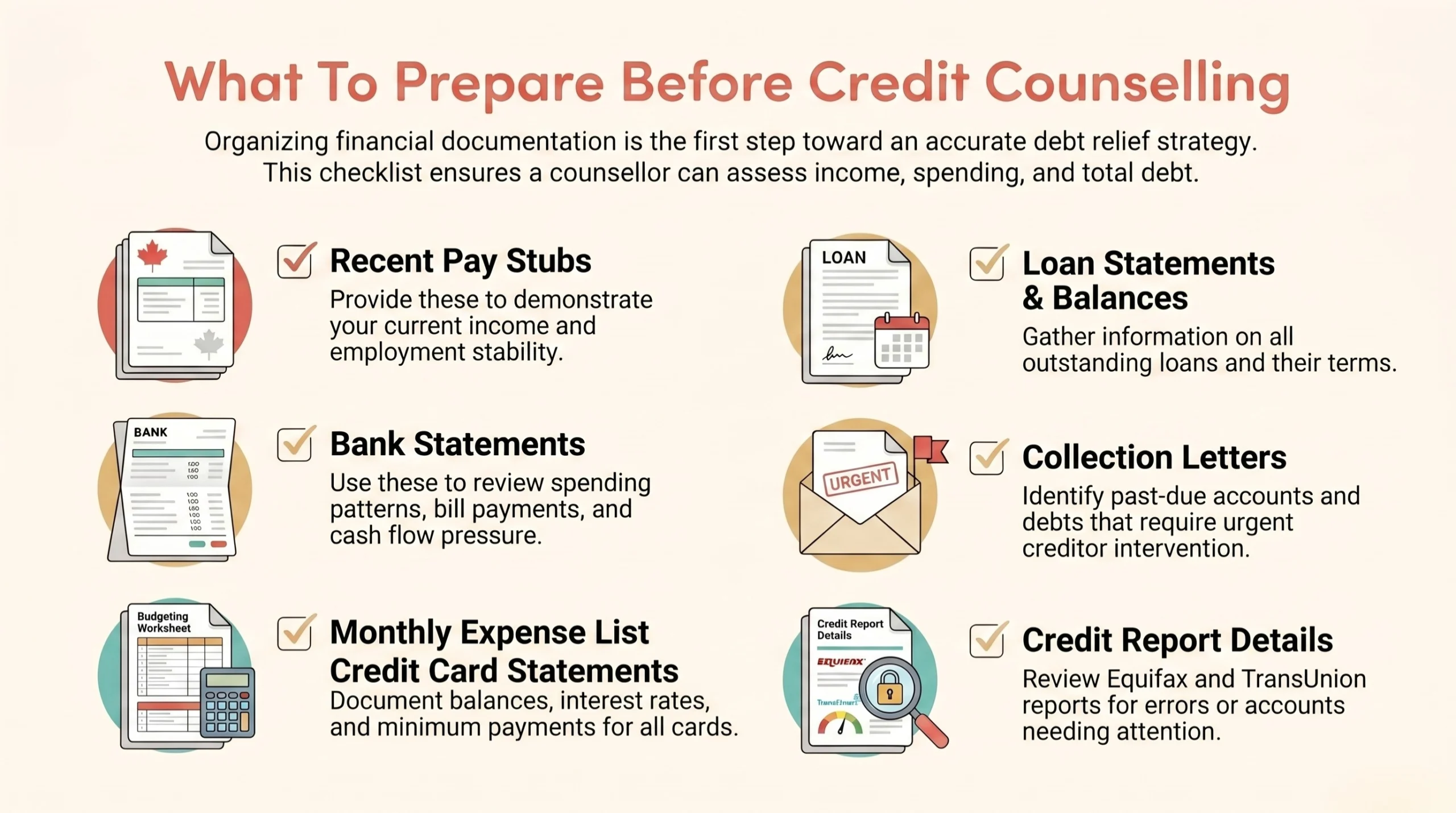

Expert Tips Before Booking Credit Counselling

Prepare Your Documents

Before your session, gather the basic documents that show your financial situation.

- Recent pay stubs

- Bank statements

- Credit card statements

- Loan balances

- Collection letters

- Monthly expense list

- Credit report details if available

The more complete your information is, the more useful the counselling session will be.

Ask the Right Questions

Good questions help you understand your options.

- What options fit my current income

- How will each option affect my credit report

- What fees are involved

- How long will repayment take

- What happens if I miss a payment

- Can this help with collection calls

- Is debt consolidation realistic for my credit profile

A good counsellor should welcome questions and explain the answers clearly.

Avoid Unrealistic Promises

Be cautious of guaranteed credit score increases.

Also, avoid instant approval promises or companies that pressure you to sign before explaining your options.

Financial recovery is a process. A serious plan should be honest about both benefits and tradeoffs.

How to Choose a Credit Counselling Service in Canada

Check Experience and Service Fit

Look for services connected with budgeting, credit improvement, debt management, debt consolidation, and consumer proposal guidance.

Credit 720 positions its work around protecting clients’ best interests and helping people understand debt restructuring options. That type of approach matters because debt decisions should be based on the borrower’s situation, not pressure from creditors.

The right service should help you understand your choices before you commit.

Check Local Availability

Local availability can make the process easier, especially if you prefer speaking with someone who understands your region.

Credit 720 provides support in Calgary, Edmonton, Toronto, Surrey, Lloydminster, and nearby Canadian regions.

This can be helpful for people seeking location-based guidance on debt, credit reports, or repayment planning.

Check Transparency

A reliable credit counselling service should explain the details clearly.

Look for transparency around these points.

- Fees

- Repayment timelines

- Credit impact

- Risks

- Alternatives

- What happens if payments are missed

Avoid pressure-based selling. You should feel informed, not rushed.

Frequently Asked Questions

What does credit counselling do in Canada?

Credit counselling helps Canadians review their income, expenses, debts, credit reports, and repayment options. It can also support budgeting, creditor communication, and debt management planning.

Does credit counselling affect your credit score?

Speaking with a credit counsellor does not directly affect your credit score. The effect depends on what solution you choose afterward, such as a repayment plan, settlement, consumer proposal, or missed payment recovery strategy.

Is credit counselling better than debt consolidation?

Credit counselling is often better as a first step when you are unsure what you can afford. Debt consolidation may help when you qualify for a reasonable rate and can manage the new payment.

Can credit counselling help with credit card debt?

Yes, credit counselling can help you understand interest costs, minimum payment problems, budget gaps, and repayment options for credit card debt.

Can I get a mortgage after credit counselling?

It may be possible to get a mortgage after credit problems, but timing depends on your credit report, income, debt load, down payment, and the solution used. A stronger payment history improves your chances over time.

How long does it take to rebuild credit after debt problems?

Credit rebuilding can take months or years, depending on the severity of missed payments, collections, settlements, or insolvency records. Consistent payments and lower balances help support recovery.

Can credit counselling stop collection calls?

Credit counselling itself may not automatically stop collection calls. However, it can help you understand repayment options, creditor communication, and whether a formal solution is needed.

What debts can be included in credit counselling?

Credit counselling often reviews unsecured debts such as credit cards, payday loans, personal loans, lines of credit, overdrafts, collection accounts, and unpaid bills.

Conclusion

Credit counselling is not just about managing debt. It is about understanding your full financial picture, protecting your credit recovery journey, and choosing a repayment path that fits your real life.

For Canadians dealing with poor credit, high credit card balances, payday loans, missed payments, or loan approval challenges, waiting too long can make the problem harder to solve.

The right guidance can help you understand budgeting, credit reports, debt consolidation, consumer proposal options, and long-term credit improvement. Credit 720 can be a helpful resource for people who want to explore debt solutions with more clarity and less pressure.

A better financial future usually starts with one honest review of where you stand today.