Poor credit can make everyday financial life feel heavier than it should. A lower score may affect your ability to qualify for a loan, rent a home, get a credit card, or access better rates. For many Canadians, the problem builds slowly through missed payments, high balances, rising expenses, or using credit cards to cover basic needs.

That is why credit counselling matters. It helps people understand what is really happening with their money and what steps they can take to reduce the pressure. Instead of guessing, avoiding bills, or making only minimum payments, Canadians can use structured guidance to rebuild control. Credit 720 supports this process by helping people review debt, understand options, and develop stronger credit habits.

What Is Credit Counselling in Canada?

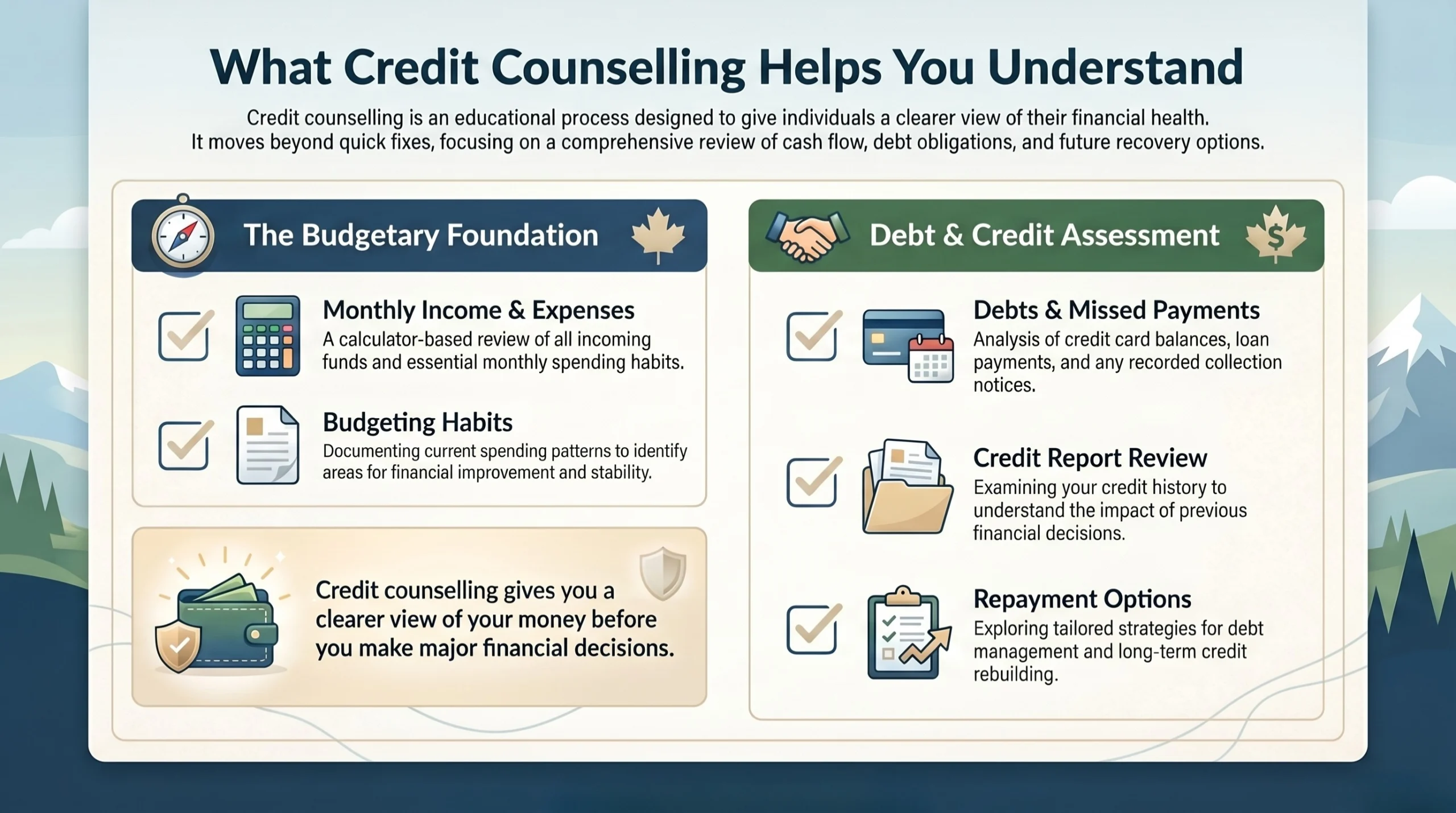

Credit Counselling in Canada is a guidance process that helps individuals understand their budget, debt, credit report, and repayment options. It is not an instant credit repair shortcut. It is a practical way to identify what is damaging your credit and what can be done next.

A credit counselling review may include:

- Monthly income and expenses

- Credit card balances and interest charges

- Missed payments or collection issues

- Budgeting habits

- Unsecured debts such as credit cards, loans, and lines of credit

- Repayment strategies that match your cash flow

For someone with poor credit, this outside perspective can be valuable. When every bill feels urgent, it is easy to focus only on the next payment. Credit counselling helps you step back and see the full financial picture.

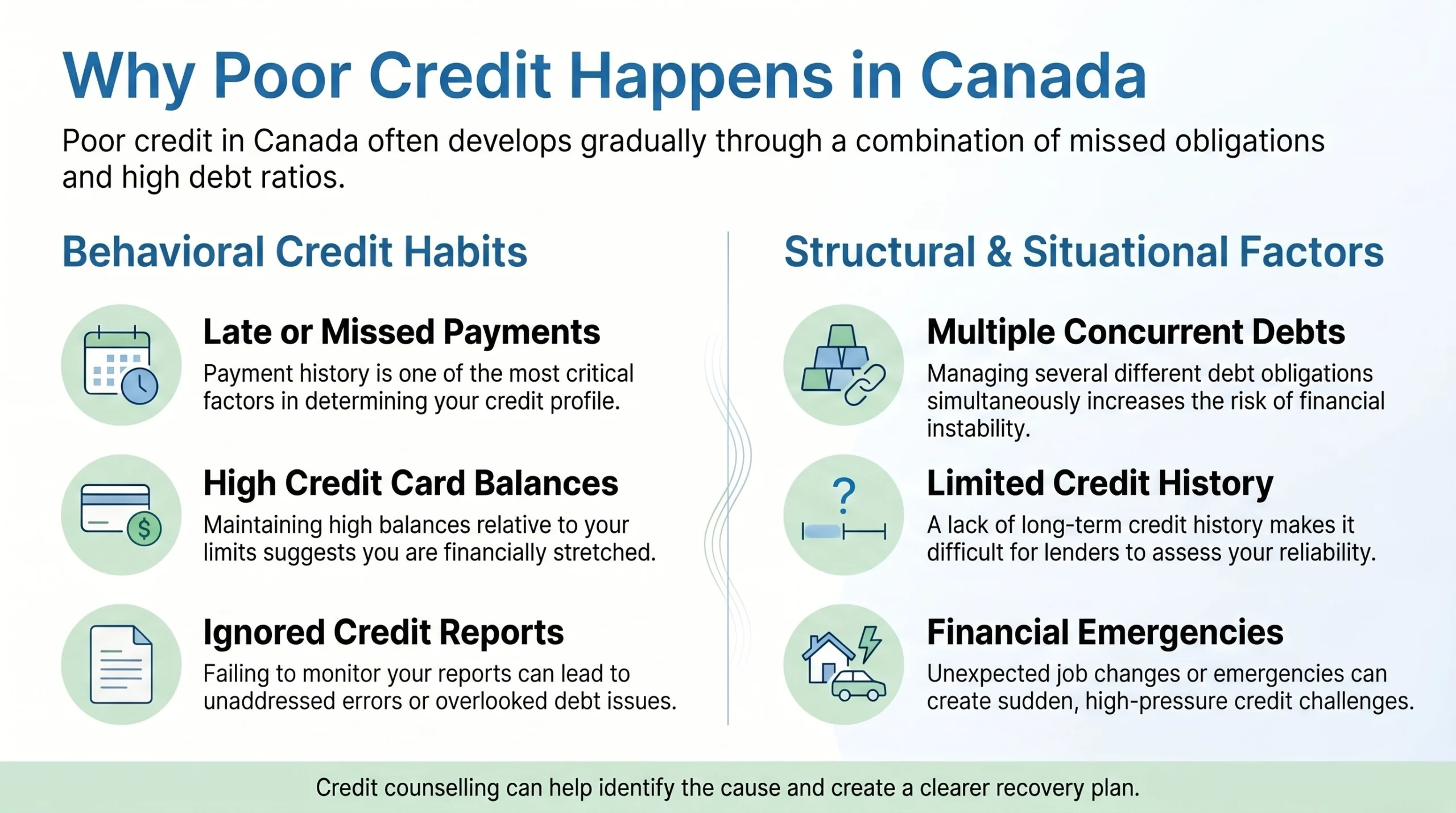

Why Many Canadians Struggle With Poor Credit

Poor credit is often linked to financial pressure, not carelessness. A person may have a steady income and still fall behind if interest charges, emergencies, or multiple payments become difficult to manage.

Late or Missed Payments

Payment history is a major factor that lenders review. Even one missed payment can create stress if it leads to fees, collection calls, or account restrictions. A better approach is to create systems that make on-time payments easier, such as automatic minimum payments, calendar reminders, and early communication with lenders.

High Credit Utilization

Credit utilization means how much of your available credit you are using. If your credit card limit is $5,000 and your balance stays near $4,500, lenders may see you as financially stretched.

Lowering balances can help your credit profile look healthier. This is why reducing credit card debt is often one of the first goals in a credit rebuilding plan.

Debt Accumulation

Credit cards, payday loans, personal loans, and lines of credit can become hard to manage when payments are spread across several accounts.

Each payment may look manageable on its own, but together they can leave little room for rent, groceries, insurance, or savings.

Why Credit Counselling Matters Before Things Get Worse

Many people wait until they are declined for credit or contacted by collectors before asking for help. In reality, credit counselling can be useful much earlier.

It can help you:

- Understand why your credit score may be low.

- Separate urgent debts from manageable debts.

- Build a realistic payment plan.

- Reduce the risk of missed payments.

- Compare debt relief options before making a major decision.

- Learn how current choices affect future borrowing.

For example, someone searching for Credit Counselling in Calgary may be juggling five credit cards and still watching balances grow. A counselling review can help identify which balances cost the most, where cash flow is leaking, and which repayment approach may be realistic.

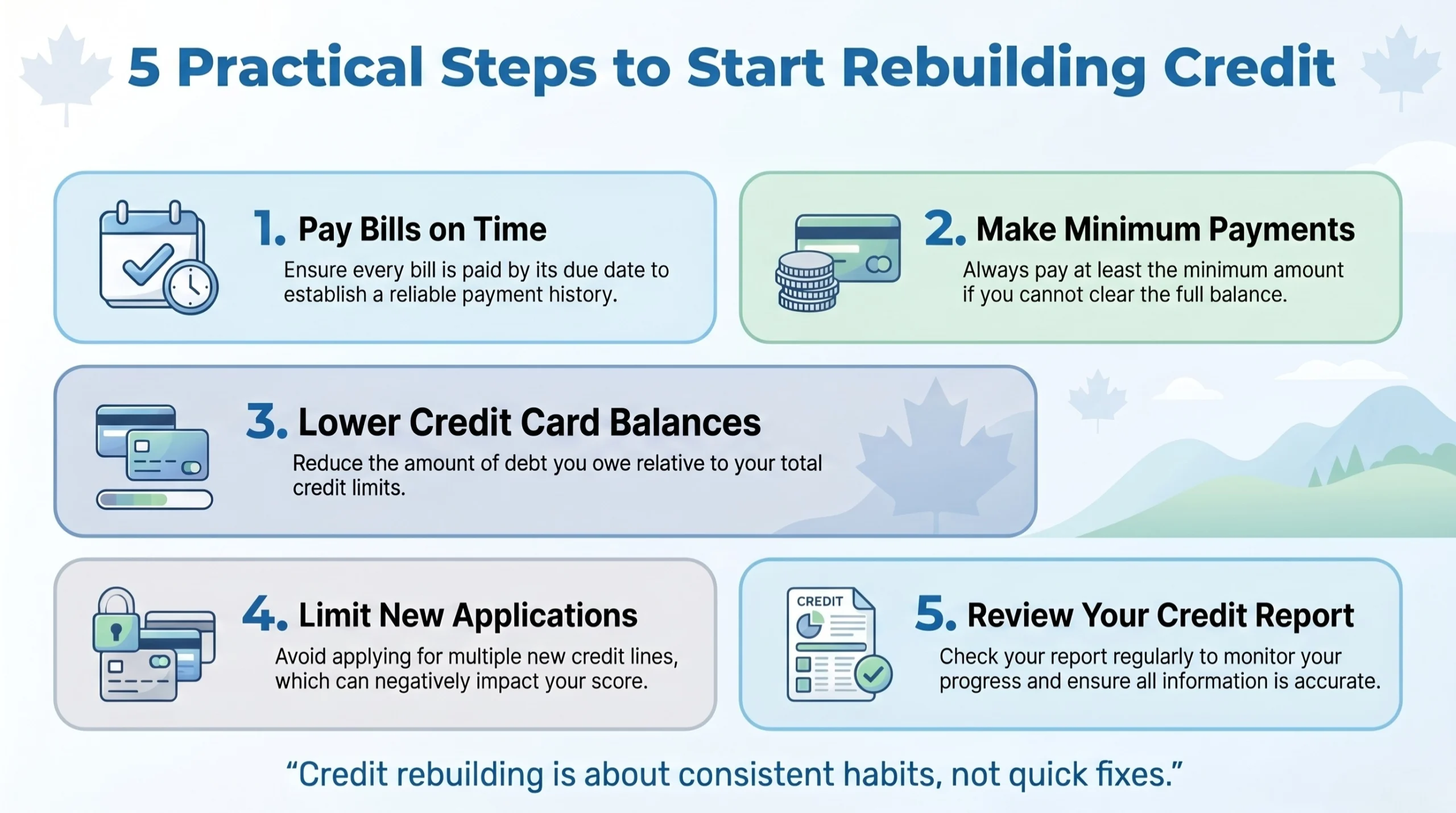

Practical Strategies to Improve Credit Over Time

Credit improvement takes consistency. The goal is not to chase a quick score increase. The goal is to build habits that make lenders see you as a lower-risk borrower.

Pay Bills on Time

If you cannot pay the full balance, make at least the minimum payment by the due date. List every bill, set reminders a few days early, and automate minimum payments where possible.

Lower Credit Card Balances

Focus on reducing balances instead of only moving debt around. You can use the avalanche method by paying high-interest debt first, or the snowball method by paying smaller balances first to build momentum. Both can work if you stay consistent.

Avoid Too Many New Applications

Applying for several loans or credit cards in a short period may make you look financially stressed. Before applying for new credit, ask whether it solves the problem or only delays it.

Review Your Credit Report

Many Canadians ignore their credit reports until they are denied financing. Reviewing your report helps you spot errors, unfamiliar accounts, outdated information, or collection items that need attention.

Build a Realistic Budget

A budget only works if it reflects real life. Include rent or mortgage, groceries, transportation, insurance, subscriptions, debt payments, savings, and irregular expenses. Credit 720 helps people connect budgeting decisions with credit rebuilding, so the plan feels practical rather than restrictive.

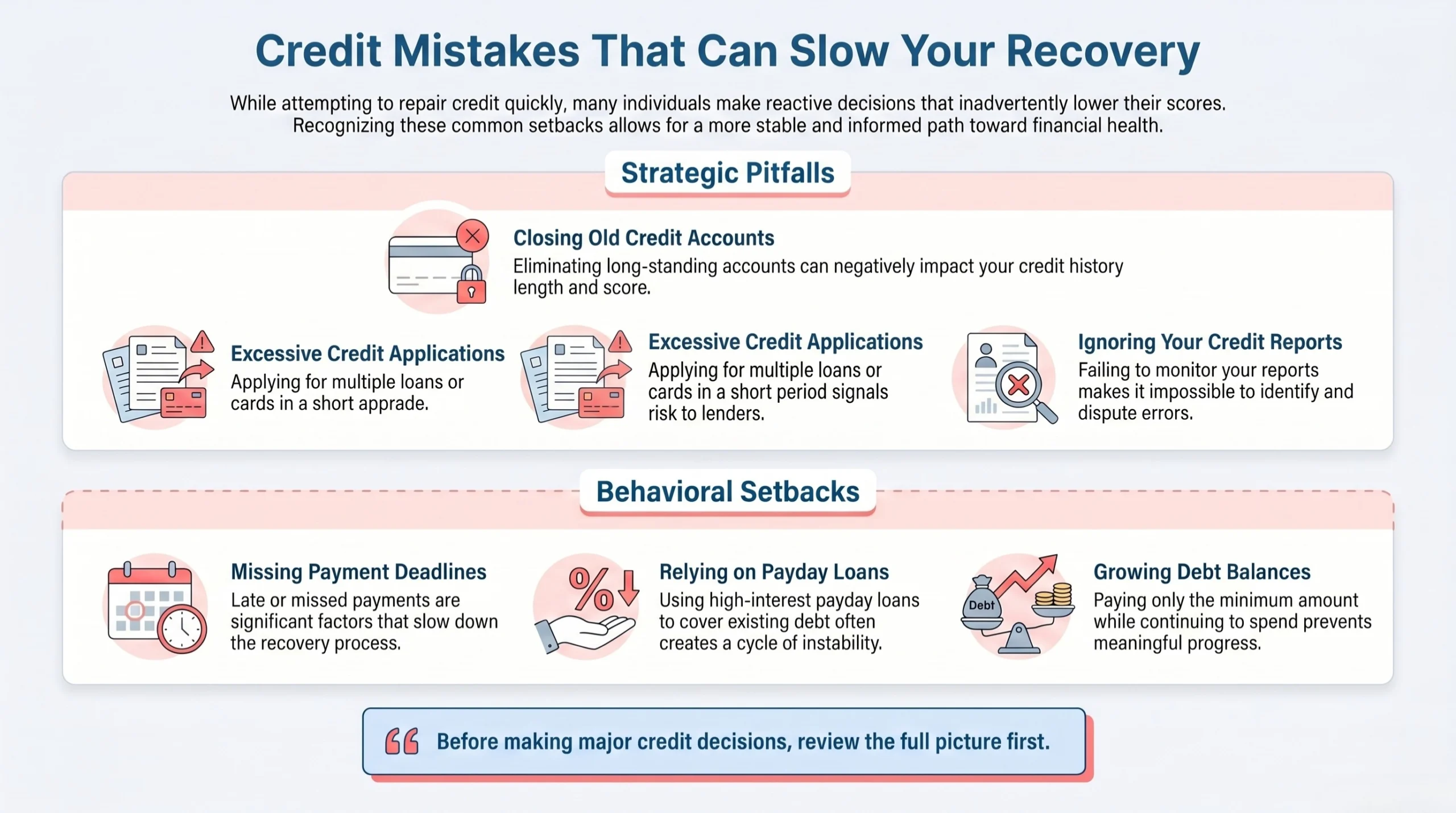

Common Credit Mistakes to Avoid

When people try to fix their credit quickly, they sometimes make choices that create new problems. Avoid closing old accounts without understanding the credit impact, paying only the minimum while still using the card heavily, ignoring collection notices, taking payday loans to cover credit card payments, or applying for multiple loans after one rejection.

One common example is closing an old credit card immediately after paying it off. That may feel responsible, but it can reduce available credit. Review the full picture before making that decision.

How Credit720 Helps Canadians Improve Credit Habits

Professional guidance can help people understand which balances to prioritize, how to organize financial documents, and when to explore structured debt solutions. When a situation requires a formal insolvency option, Canadians should understand that licensed professionals may need to be involved.

The most important benefit is clarity. Instead of reacting to pressure, you can make informed decisions that support long-term recovery.

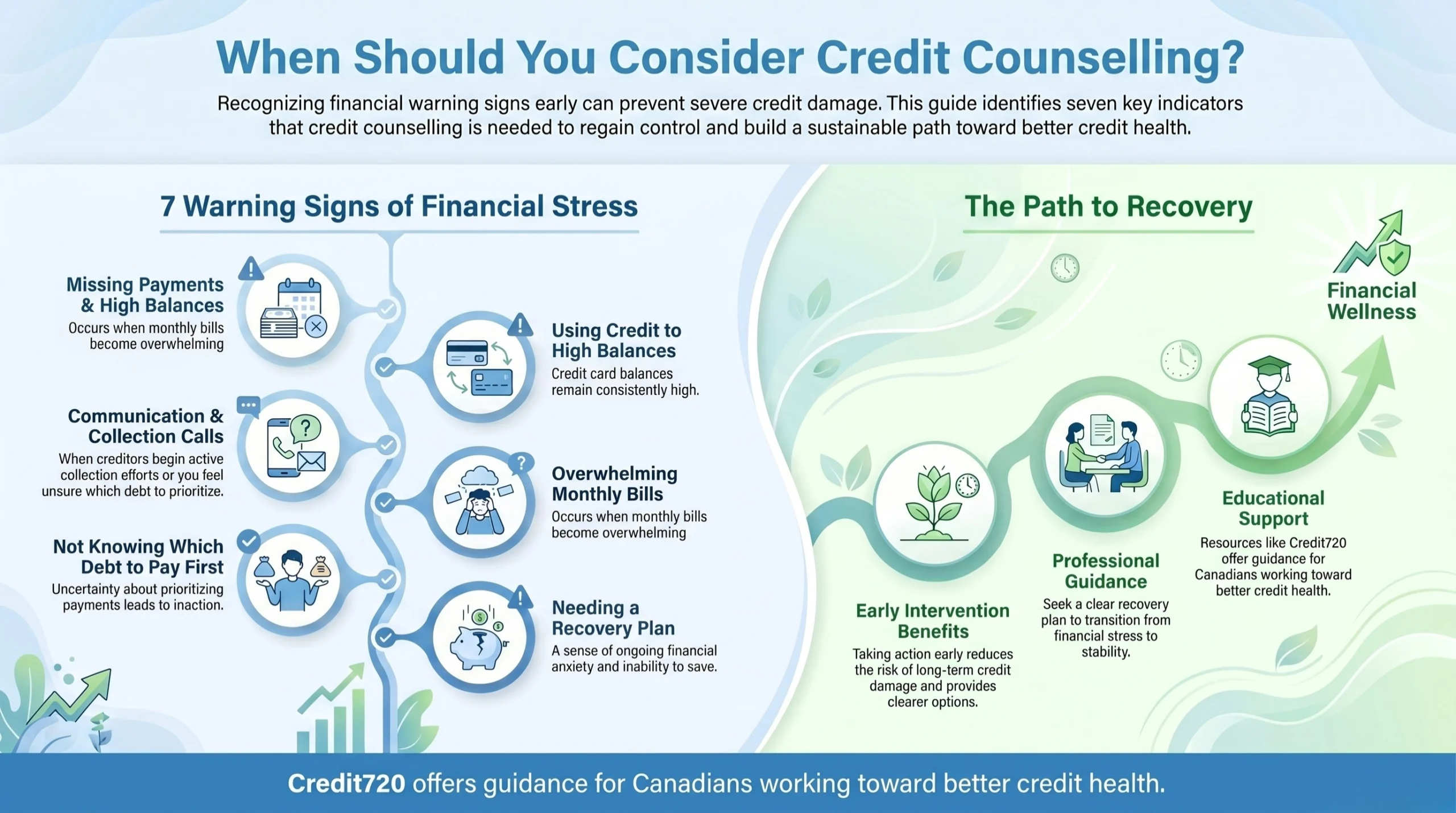

When Should You Consider Credit Counselling?

You do not need to wait until your credit score is severely damaged. Credit counselling may be useful if you are missing payments, using one form of credit to pay another, receiving collection calls, or feeling unsure which debt to pay first.

The earlier you act, the more options you may have. Even small changes, such as setting payment reminders or reducing spending leaks, can prevent further credit damage.

FAQs

What is credit counselling?

Credit counselling is guidance that helps you understand your debt, budget, credit report, and repayment options. It supports better financial decisions rather than offering an instant credit fix.

Can credit counselling improve my credit score?

Credit counselling can help you build habits that may improve your credit over time, such as paying on time and reducing balances. The actual impact depends on your payment history, debt level, and consistency.

Is Credit Counselling in Canada only for serious debt?

No. Credit counselling can help anyone who wants to understand credit, manage debt, or prevent financial problems from getting worse.

Why is Credit Counselling in Calgary helpful?

Credit Counselling in Calgary can help residents review debt, income, and repayment options practically. It is especially useful for people managing multiple payments or high-interest credit card balances.

What should I bring to a credit counselling session?

Bring recent bills, credit card statements, loan details, income information, monthly expenses, and any collection notices. Complete information makes it easier to build a useful plan.

Final Thoughts

Poor credit can feel discouraging, but it does not have to define your financial future. Most credit problems are built through repeated patterns, which means recovery also comes from repeated positive actions. Paying bills on time, lowering balances, reviewing credit reports, and getting the right guidance can help Canadians rebuild confidence step by step.

Credit counselling matters because it replaces confusion with clarity. For Canadians dealing with debt stress, poor credit, or uncertainty about repayment options, Credit 720 can be a helpful resource for education, organization, and financial recovery guidance. Explore Credit 720’s credit improvement and debt support resources before making your next financial decision.