Debt can quietly build up over time. One missed payment turns into multiple balances, credit cards stay near their limits, and suddenly, your credit score starts slipping faster than expected. For many Canadians, this becomes stressful not only financially but also emotionally. The pressure of managing several payments each month often leads to confusion, anxiety, and long-term credit damage.

This is where Debt consolidation becomes part of the conversation. Many people wonder whether consolidating debt will hurt their credit score or actually improve it over time. The truth is more balanced than most realize. While there can be short-term impacts, the long-term effects often depend on how responsibly the debt consolidation process is managed afterward.

For Canadians searching for practical financial recovery strategies, companies like Credit 720 provide guidance on debt management, credit rebuilding, and financial education designed to help people regain control of their finances without unnecessary confusion.

What Is Debt Consolidation?

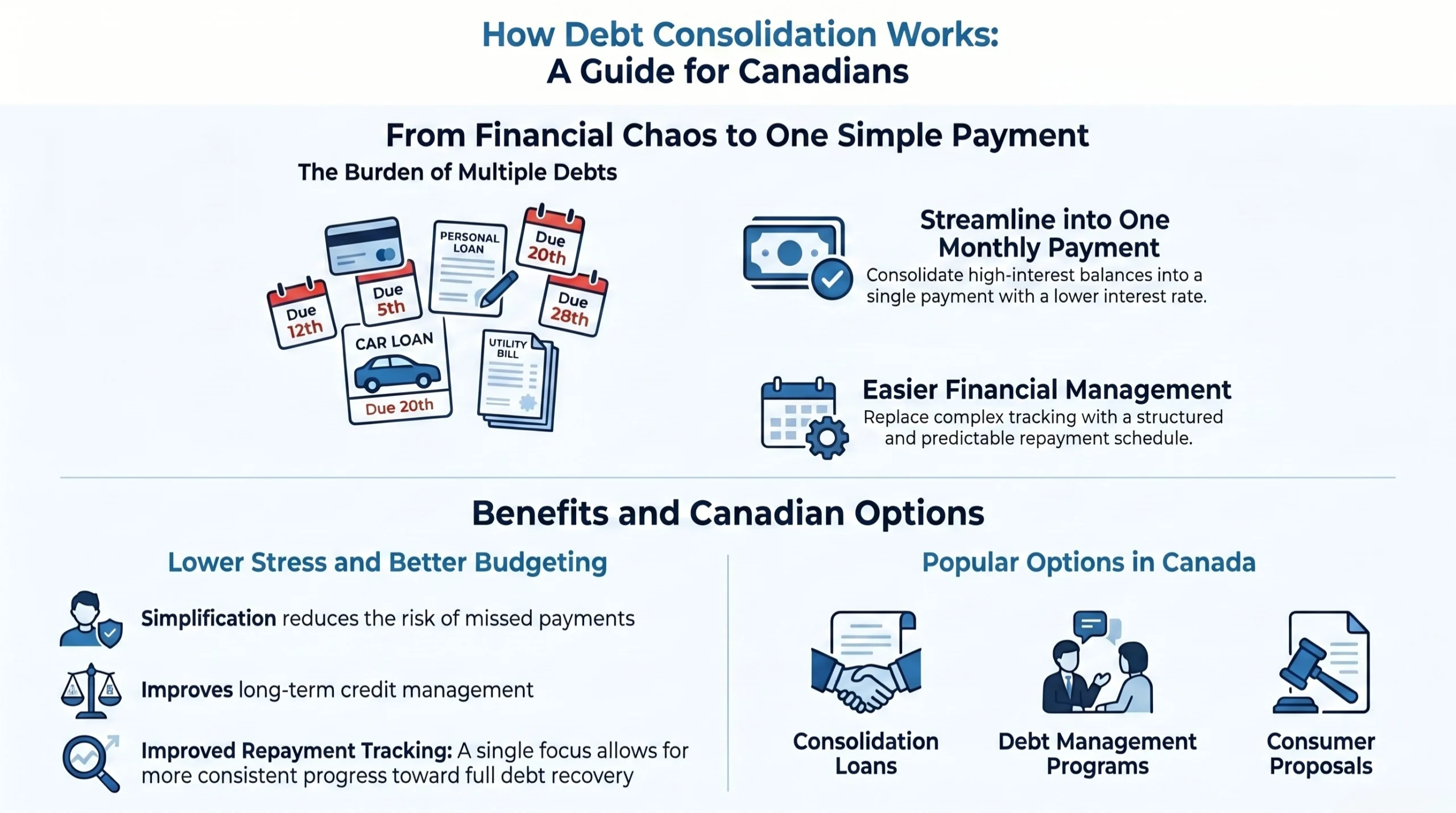

Debt consolidation means combining multiple debts into a single payment. Instead of managing several credit cards, personal loans, or high-interest balances, borrowers consolidate everything into one structured repayment plan.

Common debt consolidation methods include:

- Personal consolidation loans

- Balance transfer credit cards

- Home equity loans

- Debt management programs

- Consumer proposals

The main goal is usually to:

- Lower monthly payments

- Reduce interest rates

- Simplify repayment

- Improve financial organization

Many Canadians exploring Debt consolidation in Edmonton or Debt consolidation in Calgary are often looking for ways to reduce financial pressure while protecting or rebuilding their credit score over time.

Does Debt Consolidation Hurt Your Credit Score?

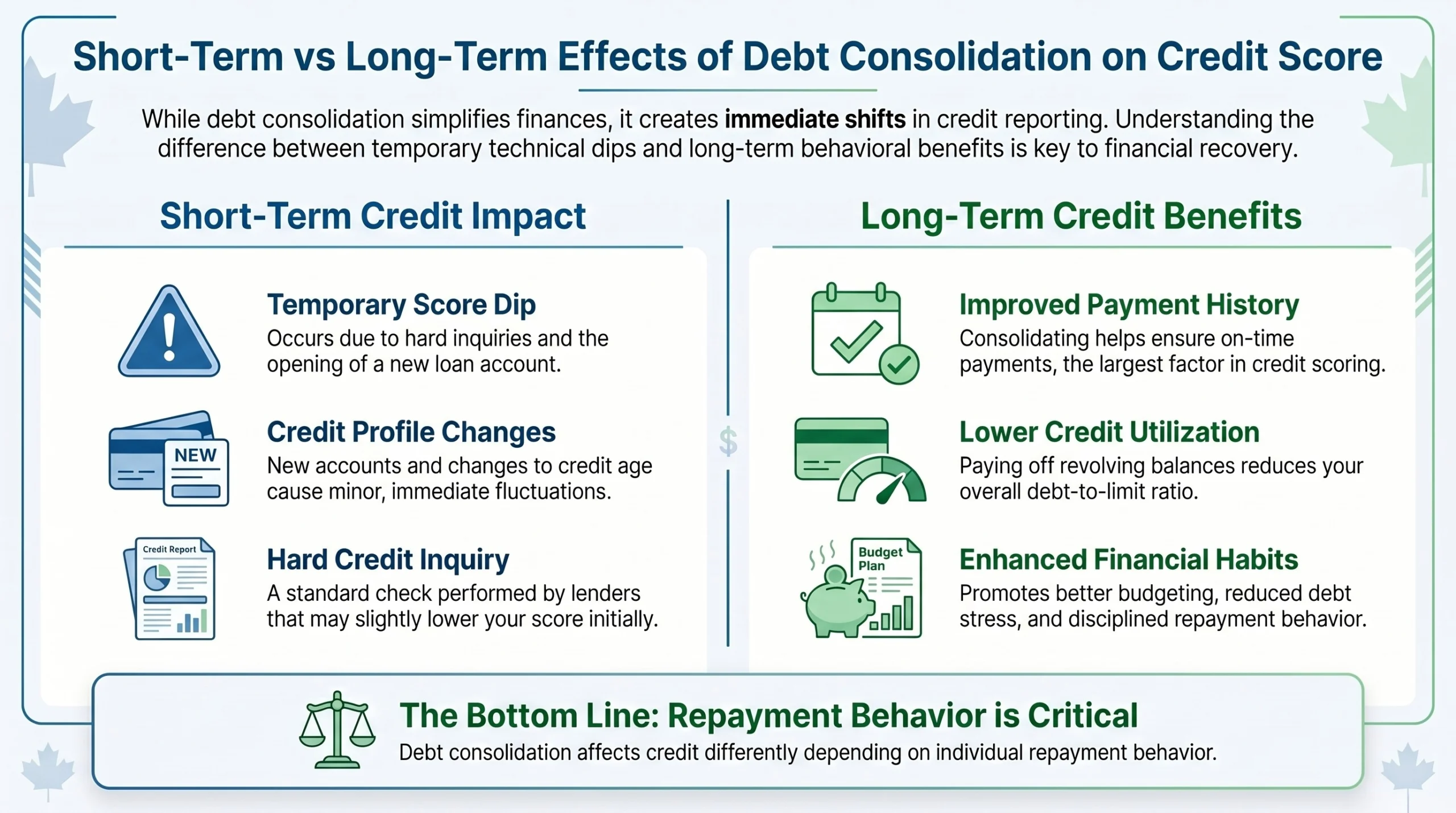

The short answer is: sometimes temporarily, but often positively in the long run.

Your credit score may dip slightly during the early stages of debt consolidation because lenders may perform a hard credit inquiry when reviewing your application. Opening a new loan account can also temporarily affect the average age of your credit history.

However, these impacts are often small compared to the long-term benefits of consistent repayment and reduced credit utilization.

Short-Term Effects on Your Credit

You may notice temporary score changes due to:

- Hard credit checks

- Opening a new credit account

- Closing old accounts too quickly

- Changes in credit mix

These effects are usually temporary if payments continue on time.

Long-Term Effects on Your Credit

Over time, debt consolidation can help improve your score by:

- Lowering credit utilization

- Reducing missed payments

- Creating a consistent payment history

- Helping manage debt more efficiently

Financial experts at Credit 720 often emphasize that payment behavior after consolidation matters more than the consolidation itself.

Why High Debt Damages Credit Scores

Before understanding how consolidation helps, it’s important to know why debt negatively affects credit scores in the first place.

High Credit Utilization

Credit utilization refers to how much of your available credit you are using. If your credit cards are constantly near their limits, lenders may view you as financially overextended.

Example:

- Credit limit: $10,000

- Balance used: $8,500

- Utilization ratio: 85%

Most financial professionals recommend keeping utilization below 30%.

Missed or Late Payments

Payment history is one of the largest factors affecting credit scores. Missing payments repeatedly can significantly lower your score and remain on your credit report for years.

Too Many Active Debts

Managing multiple loans and credit cards often increases the likelihood of missed due dates and financial stress.

How Debt Consolidation Can Improve Financial Health

Debt consolidation is not a magic solution, but it can create structure and predictability.

One Monthly Payment

Instead of juggling several due dates, borrowers only manage one payment. This reduces the risk of missed payments.

Lower Interest Costs

Consolidation loans often come with lower interest rates than credit cards. This means more money goes toward reducing the principal balance instead of interest.

Better Cash Flow Management

Lower monthly obligations may free up room in your budget for:

- Emergency savings

- Essential expenses

- Faster debt repayment

- Credit rebuilding efforts

Many Canadians seeking Debt consolidation in Calgary turn to financial guidance services like Credit 720 to better understand which repayment strategy aligns with their financial situation.

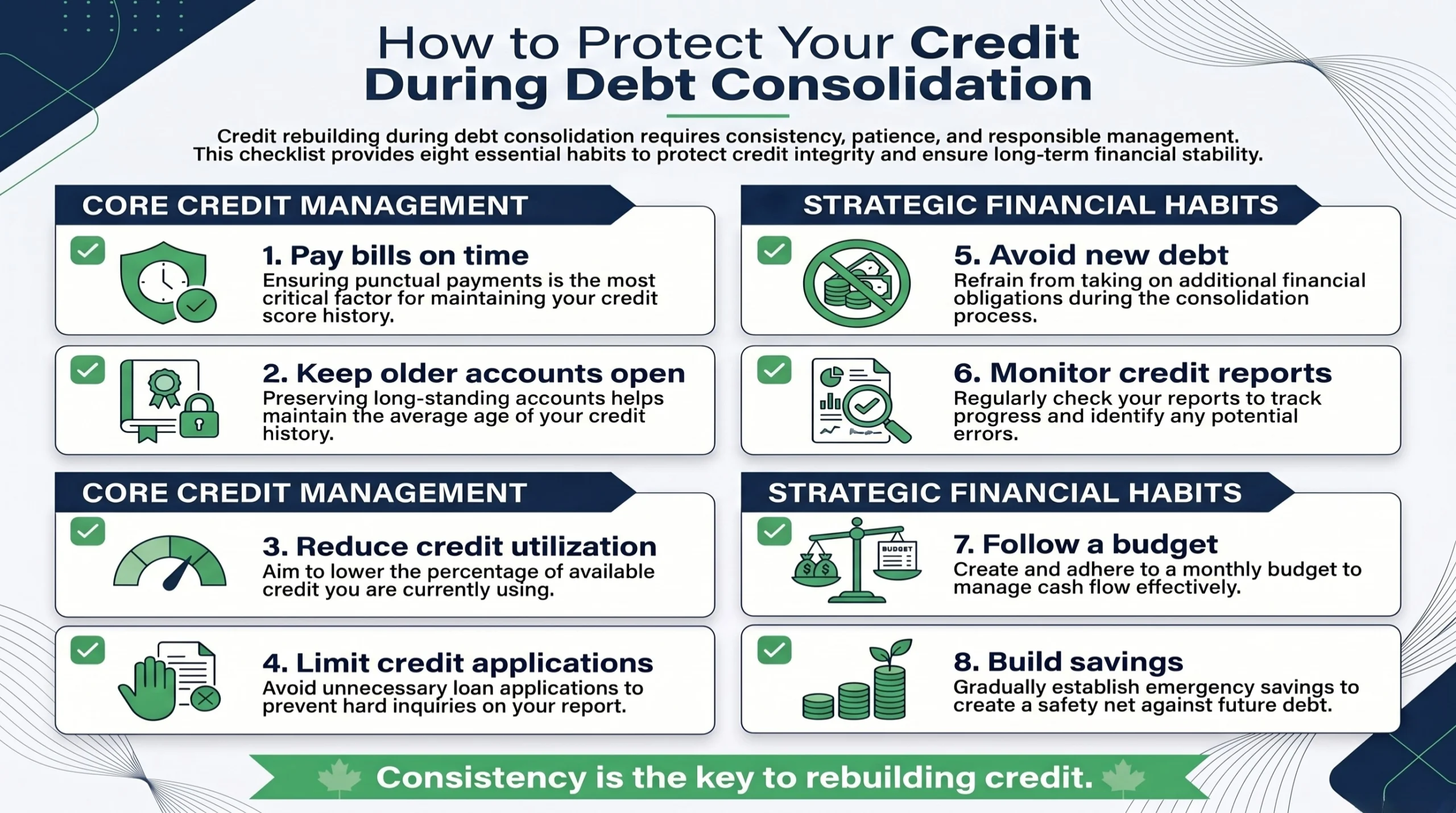

Practical Ways to Protect Your Credit During Debt Consolidation

Successfully consolidating debt requires discipline after the process begins.

1. Continue Making Payments on Time

Payment consistency matters more than almost anything else when rebuilding credit.

Helpful tips:

- Set automatic payments

- Use payment reminders

- Track monthly budgets carefully

2. Avoid Taking on New Debt

One of the biggest mistakes people make after consolidation is using old credit cards again immediately.

This creates double debt:

- Existing consolidation loan

- New credit card balances

3. Keep Older Accounts Open

Closing old accounts can shorten your credit history and increase utilization percentages.

If possible:

- Keep older cards open

- Avoid unnecessary spending

- Use cards occasionally for small purchases

4. Monitor Your Credit Report Regularly

Mistakes on credit reports happen more often than people realize.

Check for:

- Incorrect balances

- Duplicate accounts

- Payment reporting errors

- Unauthorized inquiries

Organizations like Credit 720 encourage regular credit monitoring as part of long-term financial recovery.

Common Debt Consolidation Mistakes to Avoid

Even good financial strategies can backfire if handled incorrectly.

Applying for Too Many Loans

Multiple loan applications within a short period can create several hard inquiries on your credit report.

Ignoring Budget Problems

Debt consolidation helps organize debt, but it doesn’t solve overspending habits.

Without budgeting improvements, debt may return quickly.

Missing Consolidation Payments

A consolidation loan still requires regular repayment. Missing payments can damage your score further.

Falling for Unrealistic Promises

Some companies advertise instant credit repair or guaranteed score increases. Responsible financial recovery takes time and consistent habits.

This is why many Canadians prefer educational support from experienced financial guidance providers such as Credit 720 instead of quick-fix solutions.

How Long Does It Take to Improve Your Credit Score?

Credit rebuilding timelines vary depending on:

- Current debt levels

- Payment history

- Credit utilization

- Existing collections

- Overall financial habits

Some people notice improvements within a few months, while others may need a year or longer.

Positive habits that accelerate improvement include:

- Paying every bill on time

- Reducing balances steadily

- Limiting new credit applications

- Maintaining older accounts

Consistency matters more than speed.

When Should You Consider Debt Consolidation?

Debt consolidation may be worth exploring if:

- You struggle to track multiple payments

- Interest rates are extremely high

- Credit card balances continue growing

- Minimum payments barely reduce balances

- Financial stress is affecting daily life

It may not be ideal if:

- Spending habits remain uncontrolled

- Income cannot support repayments

- Debt levels are too severe without professional intervention

Professional guidance can help determine which path makes the most sense financially.

FAQ Section

Is debt consolidation good for bad credit?

It can help simplify payments and reduce financial stress, especially when paired with consistent repayment habits and budgeting improvements.

How long does it take for debt consolidation to improve credit?

Some people notice improvements within a few months, while others may take a year or more, depending on debt levels and payment history.

Can debt consolidation stop missed payments?

Yes. Combining multiple debts into one payment often makes repayment easier to manage and reduces the risk of missing due dates.

Should I close credit cards after debt consolidation?

Not always. Keeping older accounts open may help maintain your credit history length and improve credit utilization ratios.

Final Thoughts

Debt consolidation can affect your credit score in both positive and negative ways, depending on how the process is managed. While there may be small short-term score changes, responsible repayment habits often lead to stronger long-term financial health.

The most important factor is not simply consolidating debt — it’s what happens afterward. Consistent payments, lower credit utilization, smart budgeting, and financial discipline all contribute to credit improvement over time.

For Canadians looking to better understand credit rebuilding and debt management strategies, Credit 720 offers educational guidance and financial support designed to help people make informed decisions with greater confidence.