Debt can slowly become one of the biggest sources of stress for Canadians. What starts as a few credit card balances or a temporary financial setback can eventually turn into a cycle of minimum payments, rising interest charges, and constant financial pressure. Between increasing living costs, higher borrowing rates, and unexpected expenses, many households struggle to stay ahead.

For people juggling multiple debts, keeping track of due dates and monthly payments becomes exhausting. Missing even one payment can affect your credit score, increase interest charges, and make future borrowing more difficult. This is one reason why many Canadians begin exploring debt consolidation as a way to simplify their finances and regain control.

Debt consolidation is not a magic fix, but it can create a more manageable repayment structure while reducing financial stress. When used properly, it may help improve cash flow, organize debt repayment, and support long-term credit recovery.

Understanding how debt consolidation works, who it benefits most, and when alternative debt relief solutions may be better is essential before making any financial decision.

Not sure if debt consolidation is right for you? Speak with Credit 720 specialists to explore debt relief options tailored to your financial situation.

What Is Debt Consolidation?

Debt Consolidation Definition

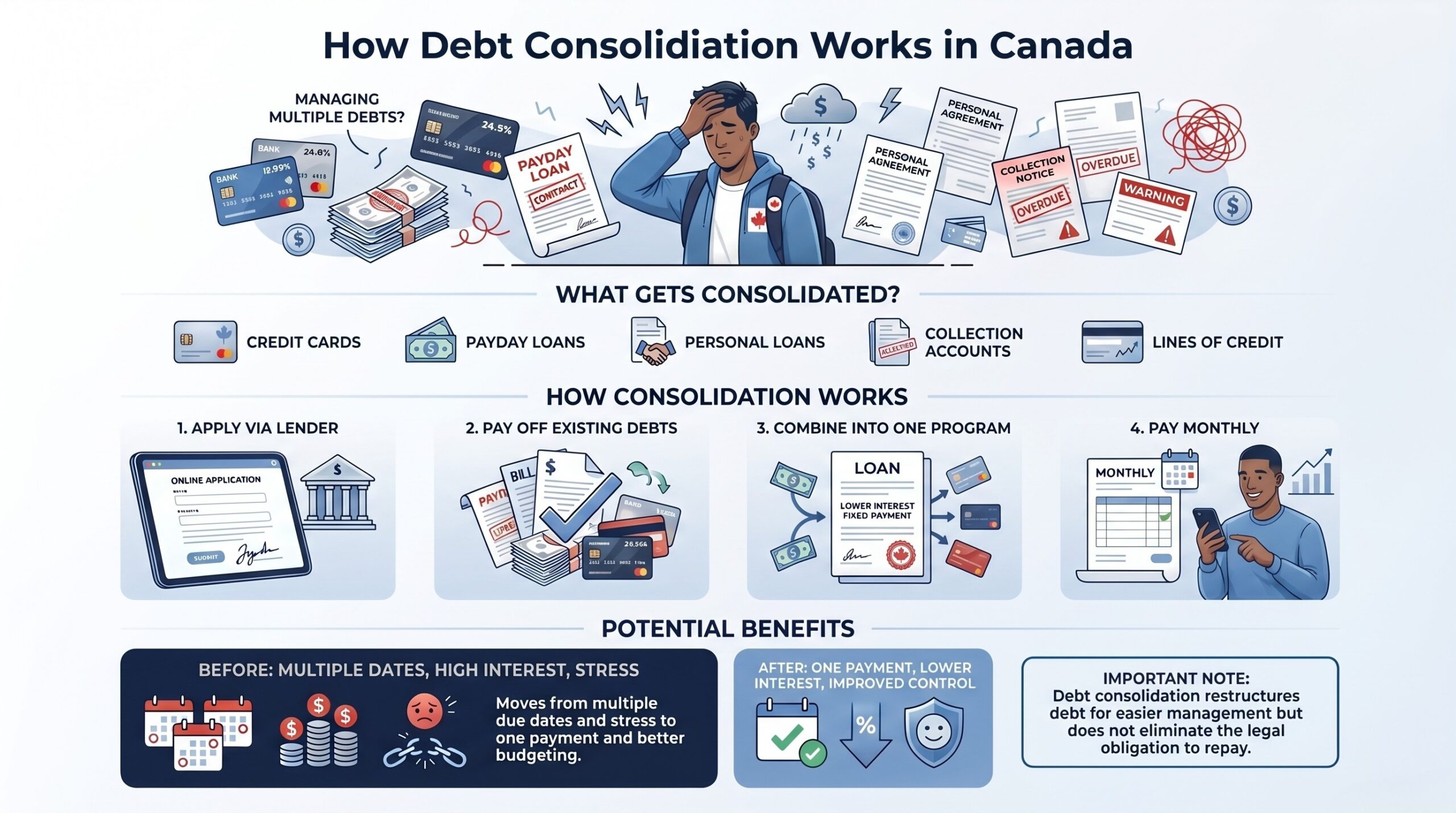

Debt consolidation is the process of combining multiple debts into one single payment. Instead of managing several credit cards, payday loans, or personal loans with different due dates and interest rates, borrowers combine them into one repayment plan.

In many cases, debt consolidation helps reduce overall interest costs or makes monthly payments easier to manage.

Common debts included in consolidation are:

- Credit card debt

- Payday loans

- Personal loans

- Lines of credit

- Collection accounts

For many Canadians, the biggest benefit is simplicity. Managing one monthly payment is often less stressful than handling five or six separate payments every month.

Debt consolidation can also:

- Improve monthly cash flow

- Reduce financial confusion

- Lower the risk of missed payments

- Create a structured repayment timeline

However, it is important to understand that debt consolidation does not erase debt. Borrowers still need disciplined repayment habits and realistic budgeting to succeed.

How Debt Consolidation Works in Canada

Debt consolidation in Canada typically involves replacing existing debts with a new loan, repayment program, or financial arrangement.

Canadians may apply through:

- Banks

- Credit unions

- Licensed credit counselling agencies

- Alternative lenders

Once approved, the new lender or program pays off the existing debts. The borrower then makes one monthly payment instead of multiple payments to different creditors.

Approval and interest rates usually depend on:

- Credit score

- Income stability

- Debt-to-income ratio

- Payment history

- Overall financial profile

For example, imagine someone carrying:

- Five credit cards

- Interest rates between 19% and 29%

- Multiple monthly due dates

By consolidating those balances into one lower-interest loan, they may reduce total interest costs while simplifying repayment into one predictable monthly payment.

Types of Debt Consolidation Options in Canada

Debt Consolidation Loans

A debt consolidation loan is one of the most common options available in Canada. A borrower receives a loan large enough to pay off existing debts and then repays the new loan through fixed monthly payments.

This option is often best for individuals with:

- Fair to good credit

- Stable income

- Consistent employment history

Benefits may include:

- Lower interest rates than credit cards

- Fixed repayment schedules

- Easier budgeting

- Clear payoff timelines

Many borrowers prefer consolidation loans because predictable payments reduce uncertainty and make financial planning easier.

Balance Transfer Credit Cards

Some Canadians use balance transfer credit cards to move high-interest debt onto a promotional low-interest or zero-interest card.

This strategy can work well for disciplined borrowers who can repay balances during the promotional period.

However, there are risks:

- Promotional rates eventually expire

- Interest rates can increase sharply afterward

- Ongoing spending may create additional debt

Without a clear repayment plan, balance transfers can sometimes worsen financial problems instead of solving them.

Home Equity Loans or HELOCs

Homeowners sometimes use home equity loans or Home Equity Lines of Credit (HELOCs) to consolidate debt.

Because these loans are secured against property, interest rates are often lower than those of unsecured loans.

This option is common among Canadians who have built significant home equity and want lower monthly borrowing costs.

Still, there are important risks:

- The home becomes collateral

- Missed payments may lead to foreclosure risk

- It may not solve deeper spending issues

Using home equity responsibly is critical when consolidating debt.

Debt Management Programs

Debt management programs are commonly offered through credit counselling agencies.

Under these programs:

- Counsellors negotiate repayment terms with creditors

- Interest reductions may be possible

- Borrowers repay debt through structured monthly plans

Many Canadians benefit from the educational side of these programs as well.

Credit counselling agencies such as Credit 720 often help clients:

- Build budgeting skills

- Understand credit reports

- Develop long-term financial recovery plans

Debt management programs can be especially useful for people dealing with moderate credit challenges who still want to repay their debts fully.

Consumer Proposals vs Debt Consolidation

Many Canadians confuse consumer proposals with debt consolidation, but they are very different solutions.

Debt consolidation reorganizes debt into one payment.

A consumer proposal legally reduces the amount of debt owed through a formal agreement with creditors.

Myth vs Fact

Myth: Debt consolidation and consumer proposals are the same.

Fact: Debt consolidation restructures repayment while consumer proposals reduce debt balances legally under Canadian insolvency laws.

Understanding the difference is important before choosing a financial solution.

Signs You May Need Debt Consolidation

Common Financial Warning Signs

Debt issues often build gradually. Some warning signs include:

- Making only minimum credit card payments

- Using one credit card to pay for another

- Frequent overdraft use

- Missing payments regularly

- Receiving collection calls

- Struggling to cover essentials

These patterns often indicate that debt has become difficult to manage independently.

Emotional and Lifestyle Indicators

Financial stress affects more than bank accounts.

Many Canadians experience:

- Anxiety when checking banking apps

- Sleep problems related to money stress

- Relationship tension caused by debt

- Constant financial worry

- Reliance on borrowing to survive monthly expenses

When debt begins affecting emotional health and daily life, seeking professional financial guidance becomes increasingly important.

How Debt Consolidation Affects Your Credit Score

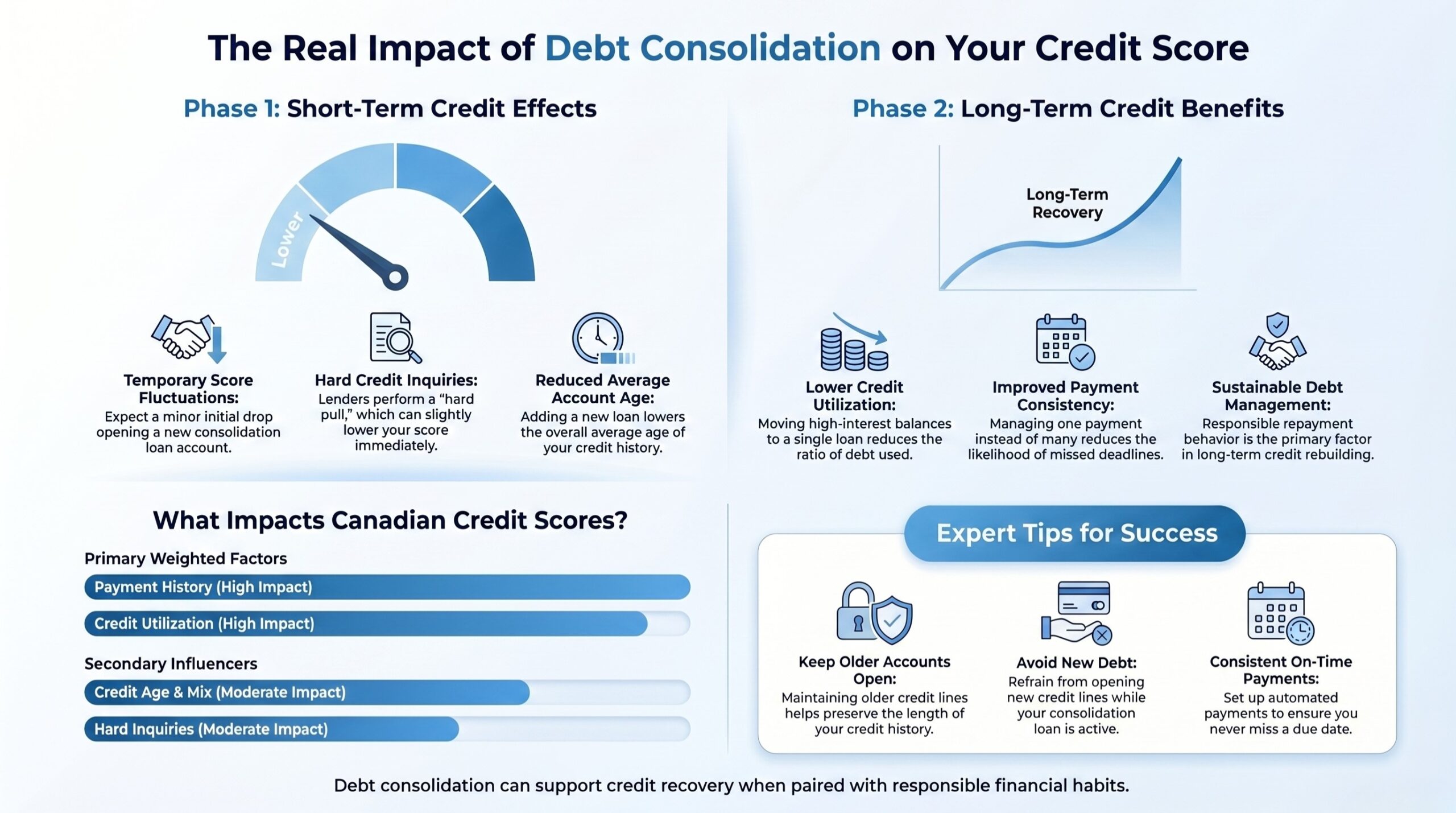

Short-Term Credit Score Impact

Debt consolidation may temporarily affect credit scores in the short term.

Potential impacts include:

- Hard credit inquiries

- New account openings

- Changes to average credit age

- Reduced available credit if accounts are closed

These effects are often temporary and manageable.

Long-Term Credit Benefits

Over time, successful debt consolidation may improve credit scores through:

- Lower credit utilization

- Consistent payment history

- Reduced missed payments

- Better account management

Many Canadians see gradual credit recovery when they consistently follow repayment plans.

Expert Tip

Keep older credit accounts open when possible and avoid taking on new debt during consolidation.

Want to improve your credit while managing debt more effectively? Learn how Credit 720 helps Canadians rebuild financial confidence while addressing debt challenges.

Credit Report Factors Canadians Should Understand

Several factors influence Canadian credit scores:

- Payment history

- Credit utilization ratios

- Length of credit history

- Credit mix

- Hard inquiries

Payment history remains one of the most important scoring factors. Missing payments consistently can significantly reduce borrowing opportunities.

Benefits of Debt Consolidation

Financial Benefits

Debt consolidation can create several financial advantages:

- Lower monthly payments

- Reduced interest costs

- Improved cash flow

- Easier budgeting

- Faster repayment potential

For borrowers struggling with high-interest credit card debt, consolidation may significantly reduce long-term borrowing costs.

Psychological Benefits

Managing multiple debts creates emotional exhaustion for many people.

Consolidation may help borrowers:

- Feel more organized

- Reduce financial stress

- Improve financial confidence

- Regain control over spending

The emotional relief of having a clear repayment strategy can be just as valuable as the financial benefits.

Loan and Mortgage Advantages

Over time, successful debt consolidation may improve mortgage and loan eligibility.

Benefits can include:

- Better debt-to-income ratios

- Improved lender confidence

- Stronger payment history

- Healthier credit profiles

Lenders often look favorably on borrowers actively managing debt responsibly.

Risks and Disadvantages of Debt Consolidation

Common Mistakes Canadians Make

Debt consolidation works best when paired with better financial habits.

Common mistakes include:

- Continuing to use credit cards excessively

- Ignoring budgeting problems

- Borrowing more than necessary

- Choosing high-interest lenders

Without behavior changes, consolidation may simply delay financial problems instead of solving them.

Debt Consolidation Scams to Avoid

Unfortunately, debt relief scams target financially stressed individuals regularly.

Warning signs include:

- Large upfront fees

- Guaranteed approval promises

- Unrealistic debt elimination claims

- Unlicensed companies

Expert Tip

Always verify licensing, reviews, and professional credentials before enrolling in any debt program.

When Debt Consolidation May Not Work

Debt consolidation is not suitable for every financial situation.

It may be less effective when someone has:

- Extremely high debt levels

- No stable income

- Ongoing borrowing habits

- Serious legal or collection issues

In these situations, alternatives such as consumer proposals or professional credit counselling may be more appropriate.

Step-by-Step Process to Consolidate Debt in Canada

Step 1: Evaluate Your Current Debt Situation

Start by listing all debts, including:

- Balances

- Interest rates

- Monthly payments

- Due dates

This creates a clear picture of your financial obligations.

Step 2: Review Your Credit Score

Check both Equifax and TransUnion reports.

Look for:

- Errors

- Outdated accounts

- Missed payment history

- Utilization levels

Understanding your credit profile helps determine which consolidation options may be available.

Step 3: Compare Consolidation Options

Compare:

- Banks versus alternative lenders

- Secured versus unsecured loans

- Interest rates

- Repayment timelines

Choosing the wrong consolidation product can increase financial stress instead of reducing it.

Step 4: Create a Repayment Strategy

Successful debt consolidation requires a long-term plan.

Focus on:

- Monthly budgeting

- Emergency savings

- Reduced unnecessary spending

- Consistent repayment habits

Get a personalized debt consolidation strategy based on your credit profile and financial goals through guidance from Credit 720.

Debt Consolidation vs Other Debt Relief Solutions

Debt Consolidation vs Credit Counselling

Debt consolidation usually involves borrowing or restructuring debt into one payment.

Credit counselling focuses more heavily on:

- Budgeting education

- Repayment planning

- Financial behavior improvements

People with moderate debt and financial management challenges often benefit from counselling support.

Debt Consolidation vs Bankruptcy

Bankruptcy carries more severe long-term financial consequences in Canada.

Potential impacts include:

- Significant credit score damage

- Asset implications

- Reduced future borrowing ability

Debt consolidation is generally less damaging to credit when repayment remains manageable.

Debt Consolidation vs Consumer Proposal

Consumer proposals offer legal debt reduction protection under Canadian insolvency laws.

Differences include:

- Legal creditor protection

- Reduced repayment amounts

- Different credit report impacts

Choosing the right option depends on debt severity, income stability, and long-term financial goals.

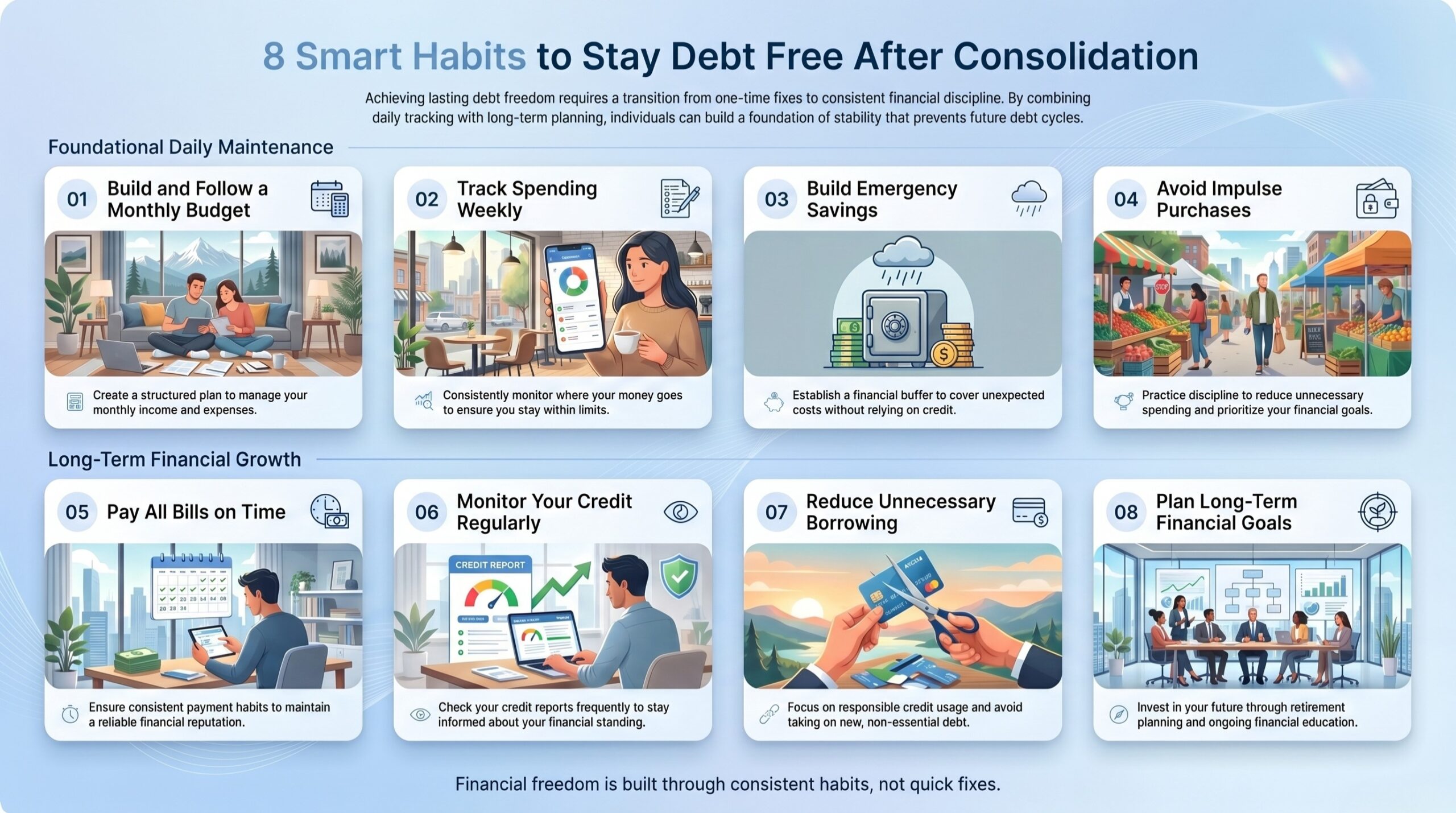

Expert Tips to Successfully Stay Debt Free After Consolidation

Build Better Financial Habits

Long-term financial recovery depends on daily habits.

Helpful strategies include:

- Following a realistic budget

- Tracking spending weekly

- Limiting impulse purchases

- Building emergency savings gradually

Small financial improvements consistently create stronger results over time.

Improve Your Credit Score Strategically

To strengthen your credit profile:

- Make all payments on time

- Keep balances low

- Avoid excessive credit applications

- Monitor reports regularly

Consistent financial discipline matters more than quick fixes.

Create a Long-Term Financial Recovery Plan

Financial recovery should extend beyond debt repayment.

Important goals may include:

- Emergency savings

- Retirement planning

- Responsible borrowing

- Ongoing financial education

Building long-term stability helps prevent future debt cycles.

Common Debt Consolidation Myths Explained

Myth vs Fact Section

Myth 1

Debt consolidation eliminates debt completely.

Fact

Debt still must be repaid. Consolidation simply restructures repayment.

Myth 2

Debt consolidation ruins credit permanently.

Fact

Responsible repayment can improve credit over time.

Myth 3

Only people with perfect credit qualify.

Fact

Some debt management and consolidation programs help borrowers with lower credit scores.

Myth 4

Debt consolidation automatically solves spending problems.

Fact

Financial habits and budgeting changes remain essential.

When Should Canadians Seek Professional Financial Help?

Situations That Require Expert Guidance

Professional support may become necessary when dealing with:

- Collection lawsuits

- Wage garnishments

- Severe financial hardship

- Repeated missed payments

- Payday loan dependency

Waiting too long can often worsen financial outcomes.

What a Credit Counsellor Can Help With

Credit counsellors can provide:

- Budgeting guidance

- Debt strategy planning

- Credit education

- Financial recovery roadmaps

Many Canadians benefit from having structured financial support during difficult periods.

Key Takeaways

- Debt consolidation combines multiple debts into one payment

- It may lower interest rates and simplify repayment

- Responsible repayment can improve credit over time

- Different consolidation options suit different financial situations

- Financial habits remain critical for long-term success

- Professional guidance may help borrowers avoid costly mistakes

Frequently Asked Questions

What is the difference between debt consolidation and debt settlement?

Debt consolidation restructures repayment into one payment, while debt settlement involves negotiating to reduce the amount owed.

Can debt consolidation improve my credit score in Canada?

Yes. Consistent payments and lower credit utilization may improve credit scores over time.

How much debt should I have before considering consolidation?

There is no exact number, but consolidation may help when multiple debts become difficult to manage comfortably.

Can I qualify for debt consolidation with poor credit?

Some lenders and debt management programs work with borrowers who have lower credit scores.

Is debt consolidation better than a consumer proposal?

It depends on the severity of debt and financial circumstances. Consolidation reorganizes debt while consumer proposals reduce balances legally.

How long does debt consolidation take to pay off?

Repayment timelines vary depending on debt size, interest rates, and monthly payment amounts.

Can debt consolidation stop collection calls?

Some debt management programs and consumer proposals may reduce or stop collection activity.

Conclusion

Debt consolidation can be a practical financial tool for Canadians struggling with multiple debts, rising interest costs, and ongoing financial stress. While it does not eliminate debt, it may simplify repayment, improve cash flow, and support long-term credit recovery when paired with responsible financial habits.

Understanding the differences between consolidation loans, debt management programs, consumer proposals, and other debt relief options is important before making any decision. Every financial situation is different, which is why personalized guidance can make a major difference.

If debt has become difficult to manage, exploring professional support and educational resources may help you regain financial stability and build a stronger financial future. Take the first step toward financial freedom with guidance from Credit 720 tailored for Canadians facing debt challenges.